This post consists of a few timeseries regression examples from my upcoming book on statistical and machine learning using Python, also to be published by Apress,as my co-authored book Python for SAS User. There are two main categories of models for time series data:

- Various variations of OLS type of regression y = a + b*x. To account for residual serial correlation, Newey-West standard errors may be used.

- Time series model, such as ARIMAX, SARIMAX

We will begin with some data analysis and then get into modeling.

Data Visualization

When we look at the timeseries data in various types of plots, we should take note of the following:

- Is mean-reverting or has explosive behavior

- Does it have a time trend

- Seasonality

- Structrural breaks

Test for Structural Breaks

It could be argued that the most important assumption of any time series model is that the underlying process is the same across all observations in the sample. Because of this, we should analyze carefully time series data with abrupt changes visually. Researching the history of the data and its context should go hand in hand with statistical analysis.

The Chow test is commonly used to test for structural change in some or all of the parameters of a model in cases where the disturbance term is assumed to be the same in both periods.

The Chow Test tests if the weights in two different regression models are the same. In other words, it tests if the model before the possible break point is the same as the model after the possible break point. The alternative hypothesis is the model fitting each periods are different.

It formally tests this by performing an F-test on the Chow Statistic which is (RSS_pooled - (RSS1 + RSS2))/(number of independent variables plus 1 for the constant) divided by (RSS1 + RSS2)/(Number of observations in subsample 1 + Number of observations in subsample 2 - 2*(number of independent variables plus 1 for the constant).

The models in each of the models (pooled, 1, 2) must have normally distributed error with mean 0, as well as independent and identically distributed errors, to satisfy the Gauss-Markov assumptions.

One of the problems of Chow’s test is that our model may detect too many breaks. In situations like this, we have to go back to the history of the data and its context, and apply judgement in combination with test results. To use Chow’s test most effecitvely, we probably should have an idea the ballpark where we want to test.

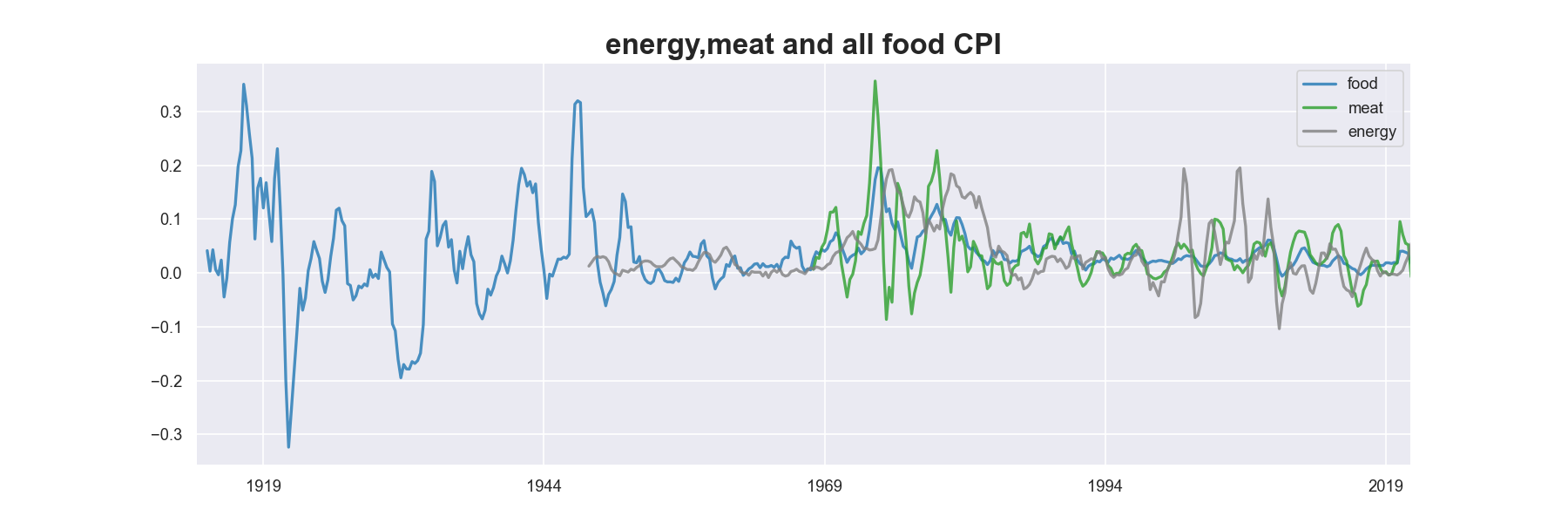

Data: Food and energy CPI

Looking at economic activity data year over year (or sometimes quarter over quarter) is a routine exercise for analysts who work with macroeconomic data, and business performance data. Tranformating the target variable using YoY often makes the time series stationary and non-serial correlated. Stationary target variable makes modeling easier because it is reduces chances of spurious regression and it is easier to isolate problems. Why? Let’s make an analogy, when you have two objects, it is easier to see what is happening if you keep one object relatively fixed (stationary) instead of both are moving.

Food and energy (along with housing) are the most important factors in daily life. We use CPI data from FRED for our first example, using .to_frame().join([meat,energy]) to combine the three time series together: urban meat prices, all food prices, and energy prices.

To avoid seeing too much volatility, we first convert the monthly data to quarterly by using .resample(‘Q’).mean(), then chain it with .pct_change(4). This gives us a quick way to compare a few time series in year over year change.

pd.options.display.float_format = '{:10,.1f}'.format

fred = fred(api_key='your key')

from fredapi import Fred as fred

import matplotlib.pyplot as plt

import seaborn as sns

sns.set()

meat=fred.get_series('CWSR0000SAF112')

meat.name ='meat'

food=fred.get_series('CPIUFDNS')

food.name = 'food'

energy=fred.get_series('CUSR0000SEHF')

energy.name = 'energy'

title = "energy,meat and all food CPI"

df = food.to_frame().join([meat,energy]).resample('Q').mean().pct_change(4)

df.plot(figsize=(15,5), alpha=0.8, linewidth=3)

plt.title(title)

# plt.savefig(r".\TimeSeries\images\food_cpi.png")

plt.show()

Data Transform

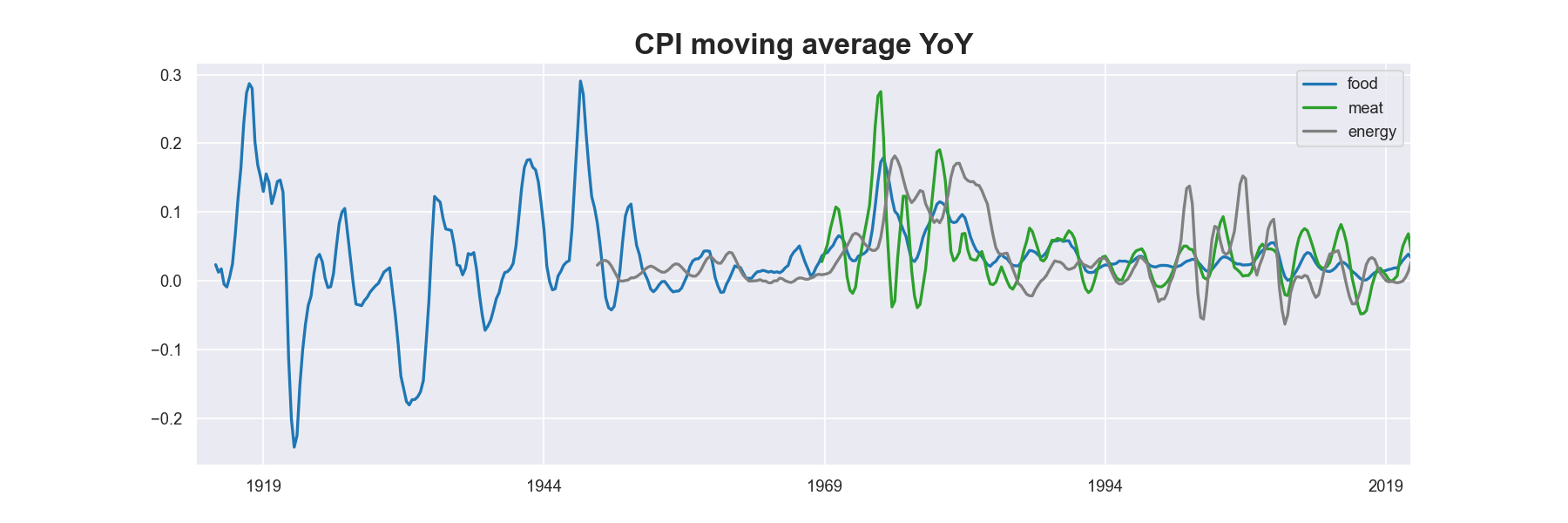

A variation of YoY transformation is moving average YoY, which first takes moving average before computing year over year. Only one line of code is need to accomplish this. Again, .resample(‘Q’).mean() changes frequency of the data from monthly to quarterly. .rolling(4).mean() takes four-quarter moving average, followed by .pct_change(4) to make it year over year change.

title = "CPI moving average YoY"

food.to_frame().join([meat,energy]).resample('Q').mean().rolling(4).mean().pct_change(4).plot(figsize=(15,5),linewidth=2, color=[blue, green,'grey'])

plt.title(title,fontdict={'fontsize': 20, 'fontweight': 'bold'})

If we have many series and cannot plots them in one chart, we may want to use the following code. To make the plots more informative, we can annotate them with statistics such as historical mean. </span> takes four-quarter moving average, followed by .pct_change(4) to make it year over year change.

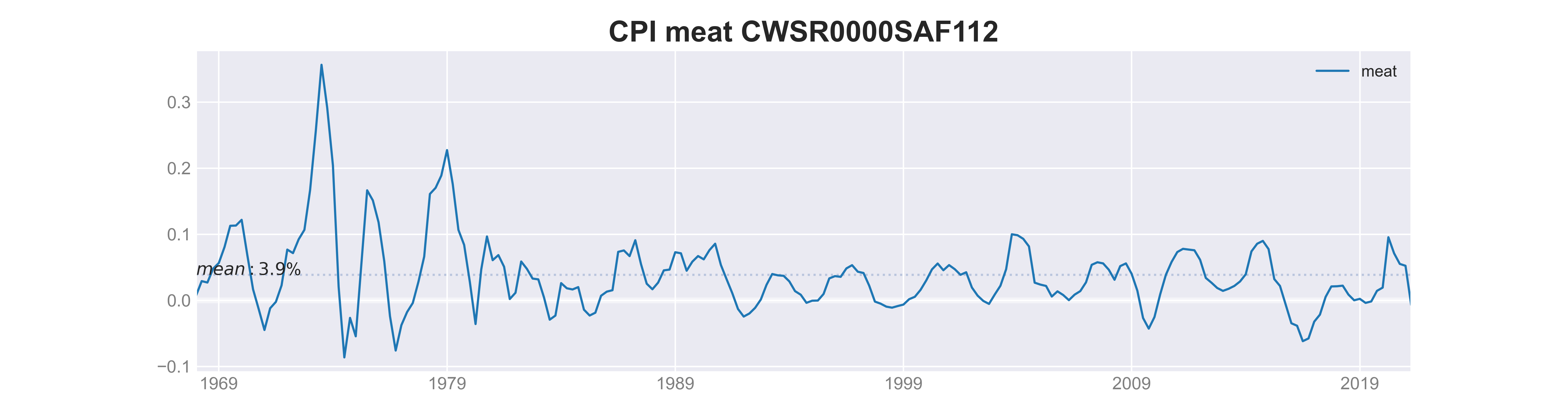

fred_series = ['CWSR0000SAF112','CPIUFDNS','CUSR0000SEHF' ]

series_names = ['meat','food','energy']

series_dict = dict(zip(fred_series,series_names))

# get series together and save them in a dataframe

s_list =[]

for i in fred_series:

s = fred.get_series(i)

s_list.append(s)

s_df = pd.concat(s_list, axis=1) #convert a list of series to dataframe

s_df.columns=series_names

# transform the entire dataframe

s_yoy =s_df.resample('Q').mean().pct_change(4)

MEAN = s_yoy.mean()

for i in fred_series:

NAME = series_dict[i]

title = "CPI " + NAME + ' '+ i

fig, ax = plt.subplots(1,1)

s_yoy[NAME].dropna(axis=0).plot(label=NAME,color=blue, ax=ax)

left_pos = s_yoy[NAME].first_valid_index()

right_pos = s_yoy[NAME].last_valid_index()

plt.hlines(MEAN[NAME], xmin=left_pos,xmax=right_pos, linestyles=":", alpha=0.3)

# annotate with historical mean

ax.text(s_yoy[NAME].first_valid_index(),MEAN[NAME], '$mean: {:.1f}$%'.format(100*MEAN[NAME]))

plt.hlines(0, xmin=left_pos,xmax=right_pos, lw=4, alpha=0.5, color='white')

plt.legend(frameon=False)

plt.title(title)

plt.show()

Note 1. 1900 - 1914 The Gold standard and stability 2. 1915 - 1924 Inflation - World War I 3. 1925 - 1939 Deflation - Interwar instability 4. 1949 - 1970 Moderate inflation - Bretton Woods and the Dollar standard 5. 1971 - 1979 Highly variable inflation - Floating exchange rates, OPEC 6. 1980 - 2000 *Disinflation* - Greater central bank independence

deflation is a decrease in general price levels throughout an economy. Deflation, which is the opposite of inflation, is mainly caused by shifts in supply and demand. disinflation is what happens when price inflation slows down temporarily. Disinflation shows the rate of change of inflation over time.

Because time series transformation is often used in feature engineering in models, we may need to merge the transformed data with the level data.

Note When merging data back, it is important to check by looking at the data, and reading the numbers. Python is easy to use, and is also very easy to make mistake with. For example, when using .join, default method is on index, if the series have different frequency, then nothing will be merged.

df = food.to_frame().join([meat,energy]).resample('Q').mean()

yoy_df = df.pct_change(4)

ma_yoy_df = df.rolling(4).mean().pct_change(4)

df = df.join(yoy_df, rsuffix='_yoy')

df = df.join(ma_yoy_df, rsuffix='_ma_yoy')

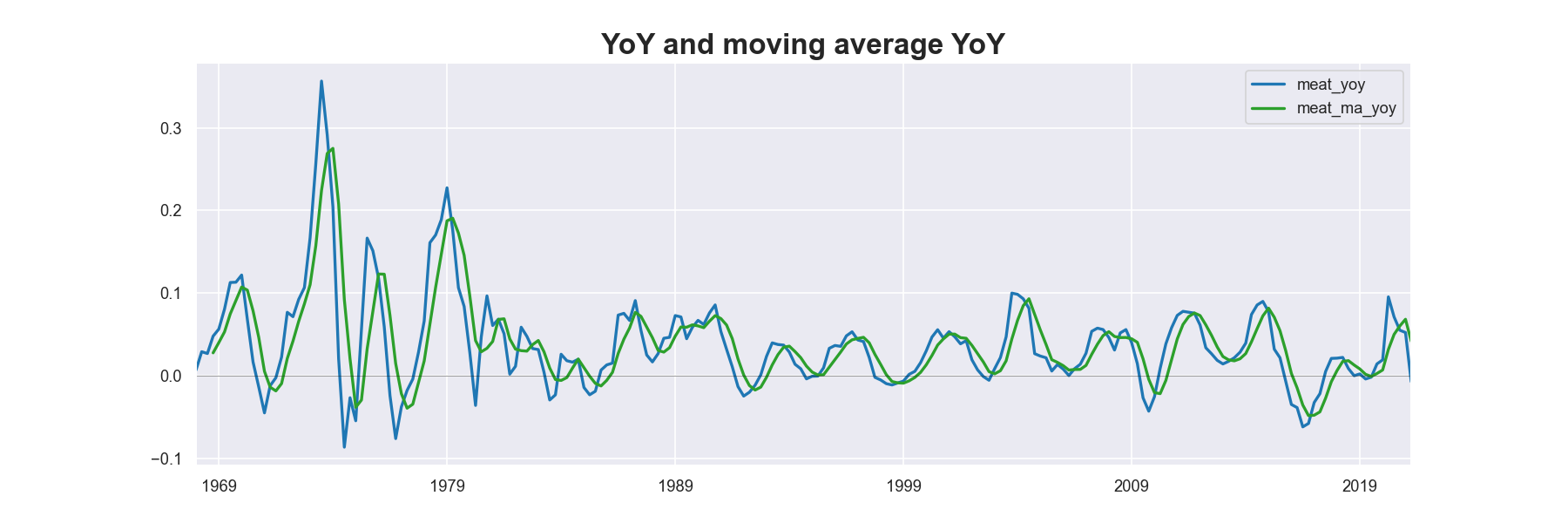

title = "YoY and moving average YoY"

df[['meat_yoy','meat_ma_yoy']].dropna(how='all',axis=0).plot(figsize=(15,5),linewidth=2, color=[blue, green])

plt.title(title,fontdict={'fontsize': 20, 'fontweight': 'bold'})

Bi-variate Plots Check for Economic Intuition

def plot_2_ts(data, x, y, year):

'''

plot 2 time series using secondary axis

y is plotted with solid blue line

x is in dotted green line

annotated with correlation

year is the beginning year

'''

temp = data.loc[str(year):, [x]+[y]].dropna(how='any', axis=0).copy()

corr = np.round(temp.corr().iloc[0,1],2)

print("corr \n",corr)

title = x + " and " + y

fig, ax1 = plt.subplots(1,1,figsize=(15,5))

ax2 = ax1.twinx()

ax1.plot(temp.index, temp[x], color=green, label=x,linestyle=":", lw=3)

ax2.plot(temp.index, temp[y], color=blue, label=y, lw=3)

ax1.set_ylabel(x, color=green)

ax2.set_ylabel(y, color=blue)

ax2.xaxis.set_major_locator(YearLocator()) #frequency

ax2.xaxis.set_major_formatter(DateFormatter('%Y'))

ax2.text(temp.index[2],temp[y].min(), "correlation = %s"%str(corr))

ax1.tick_params(axis='x', labelrotation = 90)

ax2.tick_params(axis='x', labelrotation = 90)

ax1.legend(frameon=False, loc=2)

ax2.legend(frameon=False, loc=1)

plt.xticks(fontsize=5)

plt.title(title,fontsize=20, fontweight ='bold')

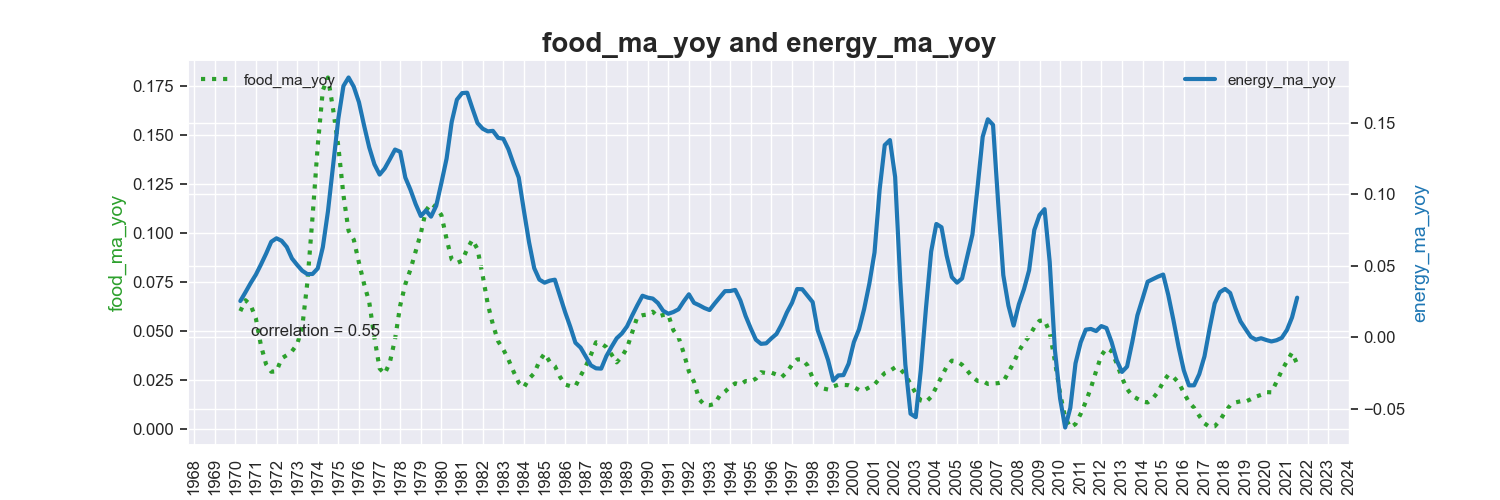

plot_2_ts(df, x= "food_ma_yoy", y = "energy_ma_yoy", year=1970)

Regression Analysis

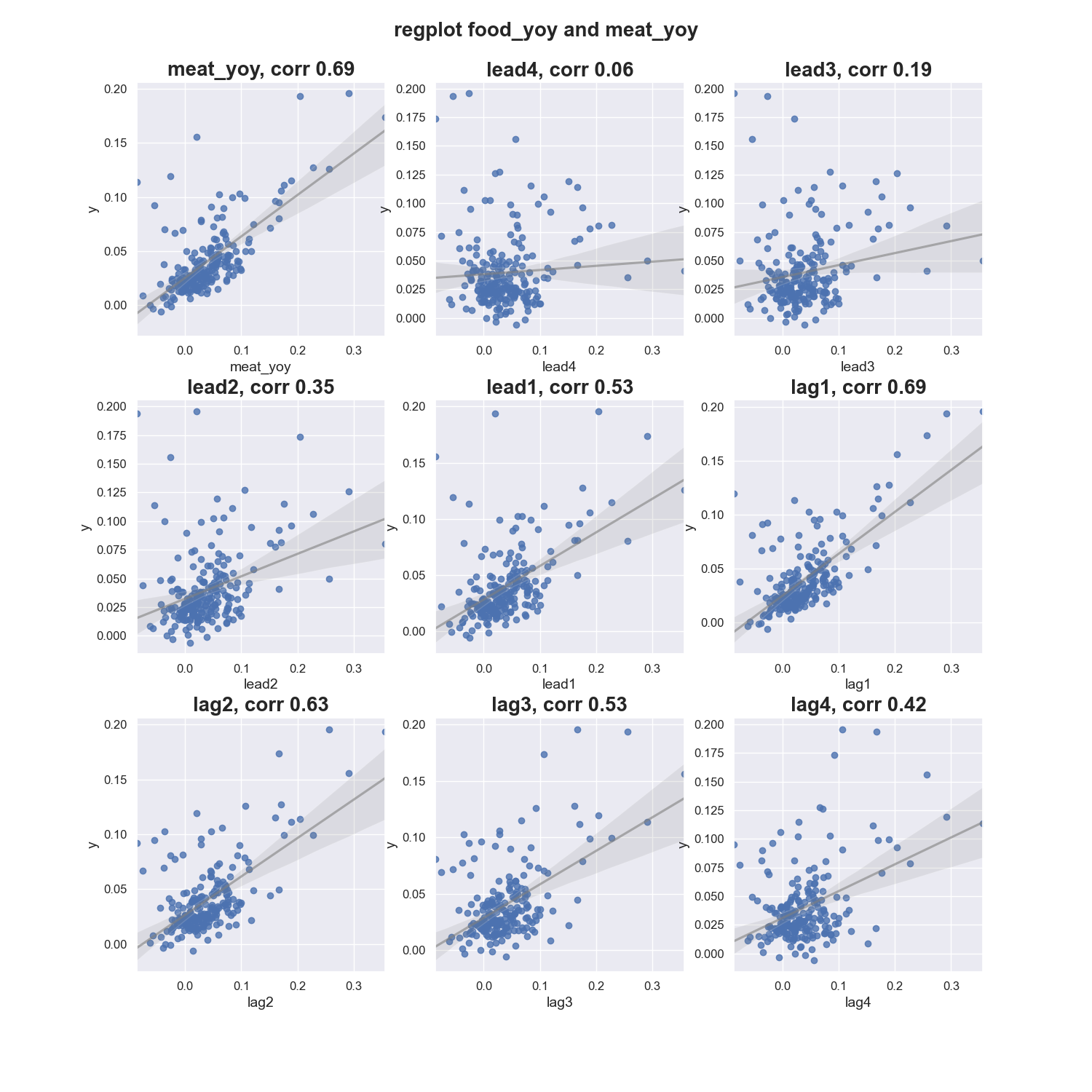

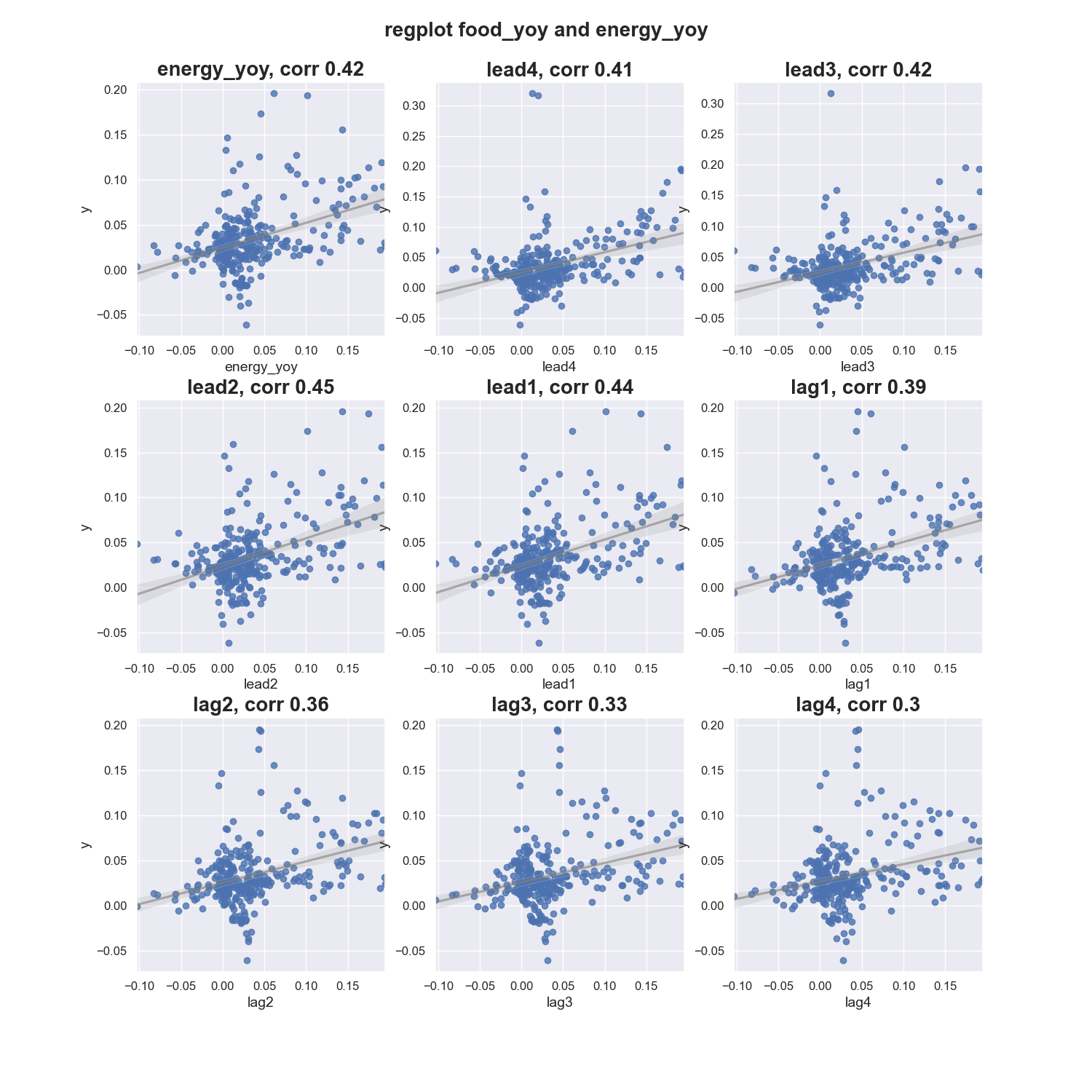

After preparing the data, we may want to do some simple regression analysis for feature selection. Below is an example that looks at various lags and leads to find which is the most correlated one with the target.

def regplots(x, y, data):

df = data[[y,x]].dropna(how='all', axis=0).copy()

df.rename({y:'y'}, inplace=True, axis=1)

df['lead1'] = df[x].shift(-1)

df['lead2'] = df[x].shift(-2)

df['lead3'] = df[x].shift(-3)

df['lead4'] = df[x].shift(-4)

df['lag1'] = df[x].shift(1)

df['lag2'] = df[x].shift(2)

df['lag3'] = df[x].shift(3)

df['lag4'] = df[x].shift(4)

corrs = np.round(df.corr()['y'][1:],2)

print("correlation is:/n", corrs)

cols = [x,'lead4','lead3','lead2','lead1','lag1','lag2','lag3','lag4']

lwargs = {'color':'grey', 'alpha':0.6}

lwargs2 = {'color':'k', 'alpha':0.6}

fig, ax = plt.subplots(3,3, figsize=(15,15))

sns.regplot(x=df[cols[0]], y=df.y, data=df, ax=ax[0,0],line_kws=lwargs).set_title("%s, corr %s"%(cols[0],str(corrs[cols[0]])))

sns.regplot(x=df[cols[1]], y=df.y, data=df, ax=ax[0,1],line_kws=lwargs).set_title("%s, corr %s"%(cols[1],str(corrs[cols[1]])))

sns.regplot(x=df[cols[2]], y=df.y, data=df, ax=ax[0,2],line_kws=lwargs).set_title("%s, corr %s"%(cols[2],str(corrs[cols[2]])))

sns.regplot(x=df[cols[3]], y=df.y, data=df, ax=ax[1,0],line_kws=lwargs).set_title("%s, corr %s"%(cols[3],str(corrs[cols[3]])))

sns.regplot(x=df[cols[4]], y=df.y, data=df, ax=ax[1,1],line_kws=lwargs).set_title("%s, corr %s"%(cols[4],str(corrs[cols[4]])))

sns.regplot(x=df[cols[5]], y=df.y, data=df, ax=ax[1,2],line_kws=lwargs).set_title("%s, corr %s"%(cols[5],str(corrs[cols[5]])))

sns.regplot(x=df[cols[6]], y=df.y, data=df, ax=ax[2,0],line_kws=lwargs).set_title("%s, corr %s"%(cols[6],str(corrs[cols[6]])))

sns.regplot(x=df[cols[7]], y=df.y, data=df, ax=ax[2,1],line_kws=lwargs).set_title("%s, corr %s"%(cols[7],str(corrs[cols[7]])))

sns.regplot(x=df[cols[8]], y=df.y, data=df, ax=ax[2,2],line_kws=lwargs).set_title("%s, corr %s"%(cols[8],str(corrs[cols[8]])))

title ="regplot %s and %s"%(y,x)

plt.suptitle(title,fontsize=20, fontweight ='bold')

plt.subplots_adjust(top=0.925, hspace=0.25)

plt.savefig(r".\Volume2\TimeSeries\images\%s.png"%title)

regplots(x='meat_yoy',y='food_yoy',data=df)

Out:

correlation is:

meat_yoy 0.690

lead1 0.530

lead2 0.350

lead3 0.190

lead4 0.060

lag1 0.690

lag2 0.630

lag3 0.530

lag4 0.420

From the correlation and regression analysis, we see that without lead or lag the correlation between food and meat is the highest.

Below plots show that food price change is more often a leading indicator for energy price change. However,

- When the target variable leads a input variable, the predicted will lag behind the actual.

- When target leads a input, we cannot no longer call the input as a “driver”, as it implies causality.

OLS Regression

We run a simple OLS regression using meat_yoy and energy_yoy to predict food_yoy.

import statsmodels.api as sm

from statsmodels.stats.stattools import durbin_watson

x1 = 'meat_yoy'

x2 = 'energy_yoy'

y = 'food_yoy'

ts = df[[x1,x2,y]].copy()

ts.dropna(how='any', axis =0, inplace=True)

X = ts[[x1,x2]].copy()

X = sm.add_constant(X)

model = sm.OLS(ts[y],ts[[x1,x2]]).fit()

model.summary()

[Out]:

OLS Regression Results

==============================================================================

Dep. Variable: food_yoy R-squared: 0.628

Model: OLS Adj. R-squared: 0.625

Method: Least Squares F-statistic: 178.5

Date: Sun, 16 May 2021 Prob (F-statistic): 4.28e-46

Time: 17:44:34 Log-Likelihood: 536.07

No. Observations: 214 AIC: -1066.

Df Residuals: 211 BIC: -1056.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0168 0.002 9.058 0.000 0.013 0.020

meat_yoy 0.3547 0.024 15.009 0.000 0.308 0.401

energy_yoy 0.2186 0.023 9.472 0.000 0.173 0.264

==============================================================================

Omnibus: 82.989 Durbin-Watson: 0.222

Prob(Omnibus): 0.000 Jarque-Bera (JB): 390.244

Skew: 1.458 Prob(JB): 1.82e-85

Kurtosis: 8.939 Cond. No. 18.3

==============================================================================

Model Evalulation 1: Residual Autocorrelation and Stationarity

From the regression results, we see that DW is 0.222. Ideally DW should be close to 2. A rule of thumb is that test statistic values in the range of 1.5 to 2.5 are relatively normal. Close to 0 DW means the residual is positively auto-correlated. Close to 4 implies negative autocorrelation.

Autoregressive relationships are very common in time series. For example, when prices are increasing, it is likely to increase for a few years. This is what some may call “momemtum”.

In context such as stock trading, strong autocorrelation shows if there is a momentum factor associated with a stock and a suitable trading strategy may be used to explore the autocorrelation.

Autocorrelation does not impact coefficient values from OLS. It impacts the estimate of the errors in significance testing. Because one of the assumptions for OLS parameter testing is independence of errors, violating this assumption makes the the standard errors smaller than they actuarlly are.

Similarly, non-stationary residual can make us underestimate standard errors of the coefficent estimates. We use augmented Dicky-Fuller test to test resdual stationarity.

from statsmodels.tsa.stattools import adfuller

stationary_test_result = adfuller(model.resid)

print('ADF Statistic: %f' % stationary_test_result[0])

print('p-value: %f' % stationary_test_result[1])

[Out]:

ADF Statistic: -2.178328

p-value: 0.214205

There are mainly three methods to correct these problems.

One of the methods to correct the problem is to use heteroskedasticity and autocorrelation consistent (HAC) standard errors such as Newey-West ( Newey, Whitney K., and Kenneth D. West. “A Simple, Positive Semi-definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix”. Econometrica 55.3 (1987): 703–708.) standard errors. By adding cov_type=’HAC’ to the fit method.

In the code below, to add the intercept term, sm.tools.add_constant(X) is used, which is equivalent to X = sm.add_constant(X) The new model summary shows that the standard errors now are larger. For example, for meat_yoy the std err went from 0.024 to 0.054. As a result, the coefficient estimate confidence intervals are wider.

X = ts[[x1,x2]].copy()

sm.OLS(ts[y], sm.tools.add_constant(X)).fit(cov_type='HAC',cov_kwds={'maxlags':2})

model.summary()

[Out]:

OLS Regression Results

==============================================================================

Dep. Variable: food_yoy R-squared: 0.628

Model: OLS Adj. R-squared: 0.625

Method: Least Squares F-statistic: 43.12

Date: Sun, 16 May 2021 Prob (F-statistic): 1.98e-16

Time: 19:24:59 Log-Likelihood: 536.07

No. Observations: 214 AIC: -1066.

Df Residuals: 211 BIC: -1056.

Df Model: 2

Covariance Type: HAC

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0168 0.002 8.954 0.000 0.013 0.021

meat_yoy 0.3547 0.054 6.629 0.000 0.250 0.460

energy_yoy 0.2186 0.058 3.751 0.000 0.104 0.333

==============================================================================

Omnibus: 82.989 Durbin-Watson: 0.222

Prob(Omnibus): 0.000 Jarque-Bera (JB): 390.244

Skew: 1.458 Prob(JB): 1.82e-85

Kurtosis: 8.939 Cond. No. 18.3

==============================================================================

Our goal is here is to get the right standard error for the coefficients. Since the p-values are extremely small even under the Newy-West errors in the presence of serial correlation and/or heteroskedasticity, we can conclude the model estimates are not significantly influenced by serial correlation and therefore appropriate for use. However, there is always a possibility that the model is not the right one for this data.

Newey-West standard errors is the simplest serial correlation corrections to implement for a simple OLS because it does not change the model if the parameters are significant. Depending on model purpose, OLS may be the preferred model, or sometimes we may prefer using a time series ARMA model to correct for autocorrelation.

Model Evaludation 2: Training Performance Testing

Before we move on to ARIMAX model, we will conduct performance testings on the OLS model.

from statsmodels.tsa.stattools import acf

def accuracy_dict_function(pred, actual):

resid =pred - actual

mape = np.mean(np.abs(resid)/np.abs(actual)) # MAPE

me = np.mean(resid) # ME

mae = np.mean(np.abs(resid)) # MAE

mpe = np.mean((resid)/actual) # MPE

rmse = np.mean((resid)**2)**.5 # RMSE

corr = np.corrcoef(pred, actual)[0,1] # corr

acf1 = acf(resid)[1] # ACF1

adf_pvalue = adfuller(resid)[1] #STATIONARY

accuracy_dict = {'mape':mape, 'me':me, 'mae': mae,

'mpe': mpe, 'rmse':rmse, 'acf1':acf1,

'corr':corr}

accuracy_dict = {key: round(accuracy_dict[key],2) for key in accuracy_dict} # dictionary comprehension to round the values

return accuracy_dict

# measure model performance

aic = np.round(model.aic)

dw = np.round(durbin_watson(model.resid),2) # 0.262

r2 = np.round(model.rsquared,2)

ts['p_yoy'] = model.predict()

ts = ts.join(df.food)

df = df.join(ts.p_yoy)

# get predicted level

df['pred'] = df['food'].shift(4)*(1+df['p_yoy'])

df.dropna(subset=['pred','food'], axis=0,inplace=True)

# performance for the backed out level variable

accuracy_dict = accuracy_dict_function(df.pred,df.food)

accuracy_dict

[Out]:

{'mape': 0.01,

'me': 0.51,

'mae': 1.77,

'mpe': 0.0,

'rmse': 2.44,

'acf1': 0.87,

'adf_pvalue': 0.34,

'corr': 1.0}

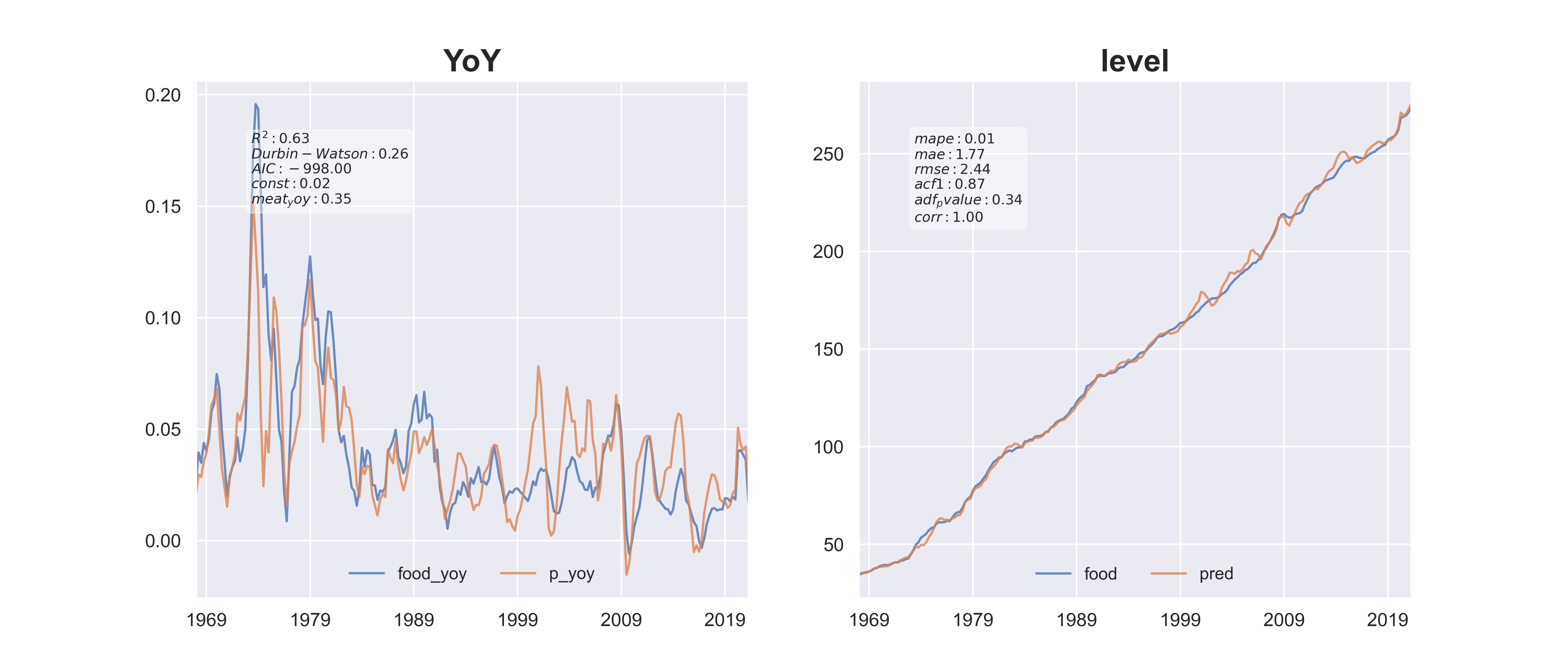

# plot

fig, ax = plt.subplots(1,2, figsize=(14,6))

df[[y,'p_yoy']].plot(ax=ax[0], title='YoY',alpha=.8)

df[['food','pred']].plot(ax=ax[1], title='level', alpha=.8)

w1 = df.index[2] #where to put text

h1 = np.min(df[y]) +0.01

# for YoY performance

textstr0 = '\n'.join((

r'$R^2: %.2f$'%(model.rsquared),

r'$Durbin-Watson: %.2f$'%(dw),

r'$AIC: %.2f$'%(aic),

r'$%s: %.2f$'%(model.params.index[0],model.params[0]),

r'$%s: %.2f$'%(model.params.index[1],model.params[1])

))

# for the level performance

textstr1 = '\n'.join((

r'$mape: %.2f$'%(accuracy_dict['mape']),

r'$mae: %.2f$'%(accuracy_dict['mae']),

r'$rmse: %.2f$'%(accuracy_dict['rmse']),

r'$acf1: %.2f$'%(accuracy_dict['acf1']),

r'$adf_pvalue: %.2f$'%(accuracy_dict['adf_pvalue']),

r'$corr: %.2f$'%(accuracy_dict['corr']),

))

textstr_lt = [textstr0, textstr1]

props = dict(boxstyle='round', facecolor='white',alpha=0.4)

for i in range(2):

ax[1].set_xlabel("")

ax[i].text(.1,.9, textstr_lt[i], fontsize=9, transform=ax[i].transAxes, va='top',bbox=props)

ax[i].legend(loc='lower center',ncol=2, frameon=False)

ARIMA Models

ARIMA Models for the Level Taget

Non-seasonal and non-stationary time series can be modeled using ARIMA. An ARIMA model is characterized by 3 terms:

- p: the order of the AR term (how many lags)

- d: the number of differencing required to make the time series stationary; use acf plot

- q: the order of the MA term

Note that ARIMA model coefficients AR(p) and MA(q) terms are bounded between (−1,1) or else the process is not stationary.

The statsmodels statsmodels.tsa.arima_model.ARIMA has the order of (p,d,q). So the first term in this ARIMA class is order of AR term, then differencing, and finally MA.

PACF (Partial Autocorrelation) plot: used for identify number of AR terms, i.e. number of lags The right order of differencing is the minimum differencing required to get a near-stationary series which roams around a defined mean and the ACF plot reaches to zero fairly quick. Adjusted Box-Tiao (ABT). In ABT, ARIMAX models with AR terms using the Box-Tiao method.

First of all, since P-value is greater than the significance level, we take difference of the series and plot autocorrelation plot. Note that because our data has datetime index, we should not use sharex=True, because datetime index and range index cannot be shared.

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.stattools import adfuller

stationary_result = adfuller(df.food_yoy)

print('ADF Statistic: %f' % stationary_result[0])

print('p-value: %f' % stationary_result[1])

[Out]:

ADF Statistic: -1.780230

p-value: 0.390320

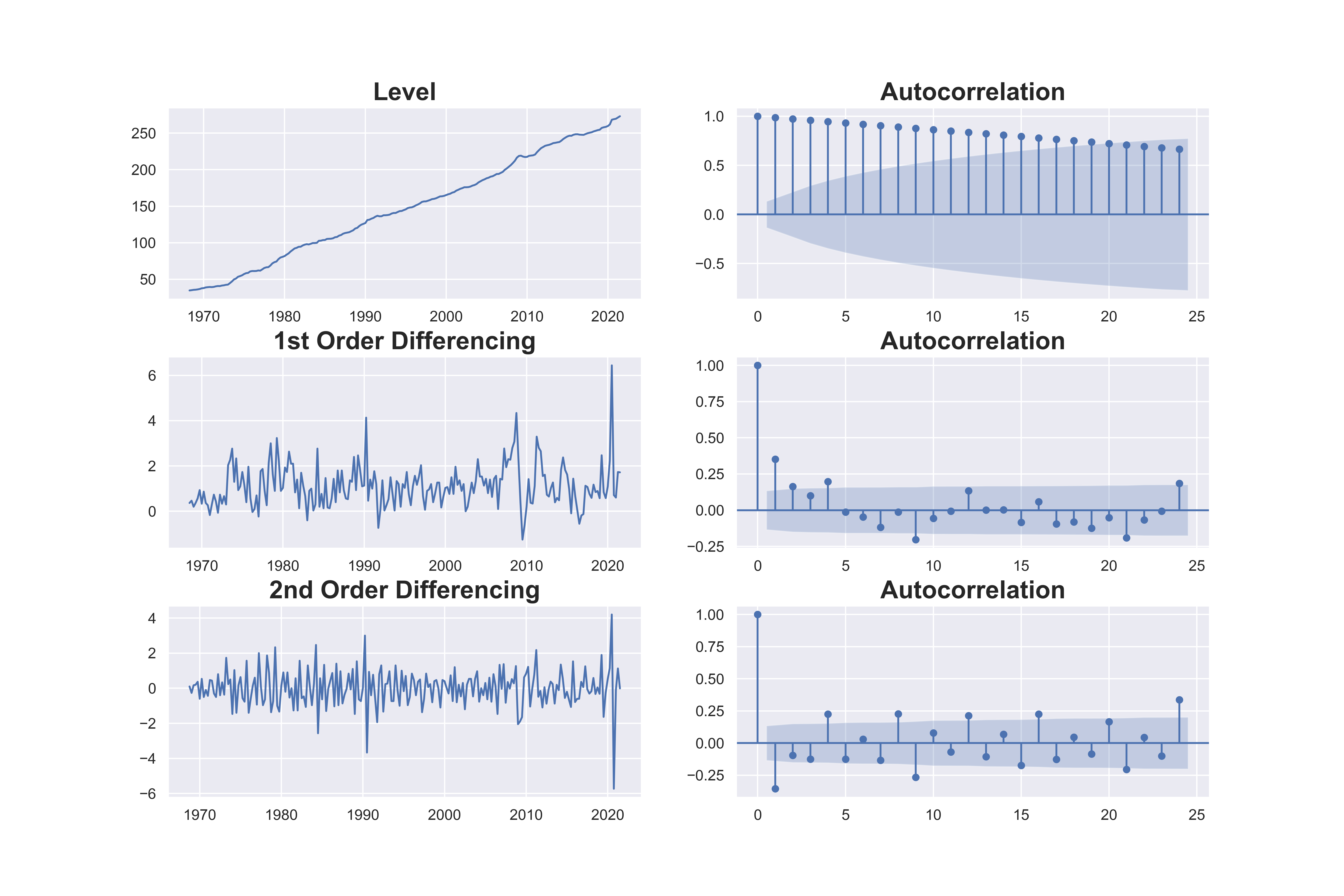

# Original Series

fig, axes = plt.subplots(3, 2,figsize=(15,10) #sharex=False

axes[0, 0].plot(df.food); axes[0, 0].set_title('Level')

plot_acf(df.food, ax=axes[0, 1])

# 1st Differencing

axes[1, 0].plot(df.food.diff()); axes[1, 0].set_title('1st Order Differencing')

plot_acf(df.food.diff().dropna(), ax=axes[1, 1])

# 2nd Differencing

axes[2, 0].plot(df.food.diff().diff()); axes[2, 0].set_title('2nd Order Differencing')

plot_acf(df.food.diff().diff().dropna(), ax=axes[2, 1])

The acf plots show that after the first difference, the autocorrelation has dropped a lot. Although there is still a bit of autocorrelation at lag 1, the first difference is better than the second difference, which went to negative correlation on the first lag. Therefore we will go with AR 1.

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.stattools import adfuller

stationary_result = adfuller(df.food_yoy)

print('ADF Statistic: %f' % stationary_result[0])

print('p-value: %f' % stationary_result[1])

[Out]:

ADF Statistic: -1.780230

p-value: 0.390320

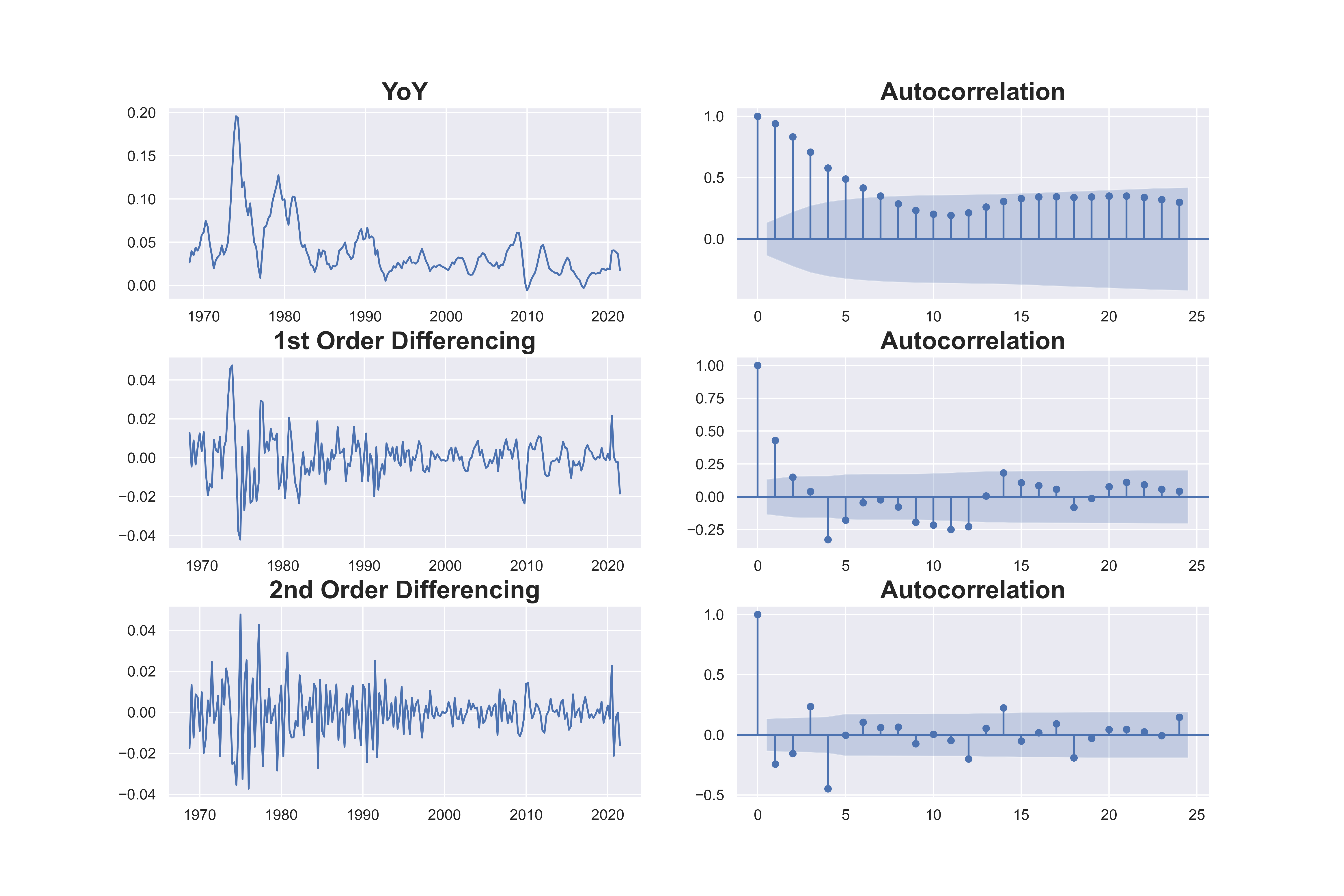

The YoY transformed autocorrelation plot is below. We see that even the YoY transformed price has strong autocorrelation in the first few lags. This is understandable because price increase/decrease don’t just last a quarter, and has momemtum effect. After the first difference, the data looks stationary but still has a little positive serial correlation at lag 1, but not severa. We will go with AR 1 as well. Besides visual examination, we can run some statistical tests as well on the number of differences needed to achieve stationarity.

The pmdarima package provides many convenient methods. Using the ndiffs from pmdarima.arima.utils we see the all three different tests agree on differencing once for food. For the YoY transformation, ADF and KPSS method concludes 1 differencing, but the PP method says no differencing is needed.

from pmdarima.arima.utils import ndiffs

y = df.food

print("ndiff by Adf Test:", ndiffs(y, test='adf'))

print("ndiff by KPSS:", ndiffs(y, test='kpss'))

print("ndiff by PP:",ndiffs(y, test='pp'))

[Out]:

ndiff by Adf Test: 1

ndiff by KPSS: 1

ndiff by PP: 1

y = df.food_yoy

print("ndiff by Adf Test:", ndiffs(y, test='adf'))

print("ndiff by KPSS:", ndiffs(y, test='kpss'))

print("ndiff by PP:",ndiffs(y, test='pp'))

[Out]:

ndiff by Adf Test: 0

ndiff by KPSS: 1

ndiff by PP: 0

We begin with an ARIMA(1,1,1) model. The ma term ma.L1.D.food is not signficant, which is dropped in the second try in an ARIMA(1,1,0) model. We notice that AIC and BIC dropped, and the p-value for ar.L1.D.food is smaller, which means the ARIMA(1,1,0) is a simpler and more robust model than ARIMA(1,1,1).

from statsmodels.tsa.arima_model import ARIMA

train = df.food

model = ARIMA(train, order=(1, 1, 0)).fit()

model.summary()

[Out]:

ARIMA Model Results

==============================================================================

Dep. Variable: D.food No. Observations: 213

Model: ARIMA(1, 1, 1) Log Likelihood -273.430

Method: css-mle S.D. of innovations 0.873

Date: Sun, 16 May 2021 AIC 554.860

Time: 15:14:31 BIC 568.305

Sample: 06-30-1968 HQIC 560.294

- 06-30-2021

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

const 1.1184 0.100 11.197 0.000 0.923 1.314

ar.L1.D.food 0.5186 0.204 2.538 0.011 0.118 0.919

ma.L1.D.food -0.1932 0.241 -0.802 0.422 -0.665 0.279

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.9283 +0.0000j 1.9283 0.0000

MA.1 5.1752 +0.0000j 5.1752 0.0000

-----------------------------------------------------------------------------

model = ARIMA(train, order=(1, 1, 0)).fit()

model.summary()

[Out]:

ARIMA Model Results

==============================================================================

Dep. Variable: D.food No. Observations: 213

Model: ARIMA(1, 1, 0) Log Likelihood -273.749

Method: css-mle S.D. of innovations 0.875

Date: Sun 16 May 2021 AIC 553.497

Time: 15:21:19 BIC 563.581

Sample: 06-30-1968 HQIC 557.572

- 06-30-2021

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

const 1.1187 0.092 12.130 0.000 0.938 1.299

ar.L1.D.food 0.3519 0.064 5.491 0.000 0.226 0.477

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 2.8419 +0.0000j 2.8419 0.0000

-----------------------------------------------------------------------------

You can find out the required number of AR terms by inspecting the Partial Autocorrelation (PACF) plot.

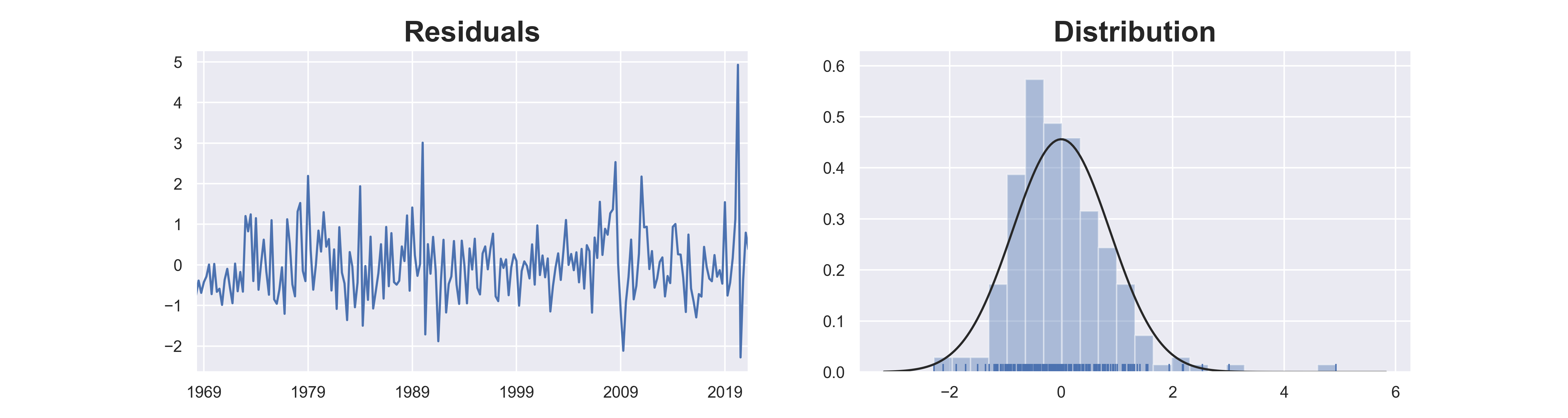

# residual

residuals =model.resid

from scipy import stats

from scipy.stats import norm

norm_test =stats.anderson(residuals, dist='norm')

stat, p = stats.kstest(residuals, 'norm')

print('p-value: {0: .4f}'.format(p))

[Out]:

p-value: 0.0958

fig, ax = plt.subplots(1,2, figsize=(15,4))

residuals.plot(title="Residuals", ax=ax[0])

sns.distplot(residuals, fit=norm, kde=False, rug=True, ax=ax[1])

plt.title("Distribution")

plt.show()

title = "ARIMA(1,1,0) non-dynamic level actual vs predicted"

model.plot_predict(dynamic=False)

The dynamic=False specification in .plot_predict uses the in-sample lagged values for prediction, which can make the predicted look better than they actually are. We will get to out-of-sample testing in the next section.

%20non-dynamic%20level%20actual%20vs%20predicted.png)

YoY ARIMA Models

Both the AR and MA terms are significant.

When we have AR 3, AIC and HQIC increased but BIC dropped slightly. We will go with AR 2 and see how the residual looks like.

from statsmodels.tsa.arima_model import ARIMA

train = df.food_yoy

model = ARIMA(train, order=(2, 1, 0)).fit()

model.summary()

[Out]:

ARIMA Model Results

==============================================================================

Dep. Variable: D.food_yoy No. Observations: 213

Model: ARIMA(2, 1, 1) Log Likelihood 693.187

Method: css-mle S.D. of innovations 0.009

Date: Mon, 17 May 2021 AIC -1376.375

Time: 18:32:01 BIC -1359.569

Sample: 06-30-1968 HQIC -1369.583

- 06-30-2021

====================================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------------

const -1.347e-05 0.001 -0.012 0.990 -0.002 0.002

ar.L1.D.food_yoy -0.3167 0.071 -4.456 0.000 -0.456 -0.177

ar.L2.D.food_yoy 0.1866 0.071 2.635 0.008 0.048 0.325

ma.L1.D.food_yoy 0.9554 0.019 49.319 0.000 0.917 0.993

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -1.6171 +0.0000j 1.6171 0.5000

AR.2 3.3147 +0.0000j 3.3147 0.0000

MA.1 -1.0467 +0.0000j 1.0467 0.5000

-----------------------------------------------------------------------------

title = "ARIMA(2,1,0) YoY actual vs predicted"

model.plot_predict(dynamic=False)

%20YoY%20actual%20vs%20predicted.png)

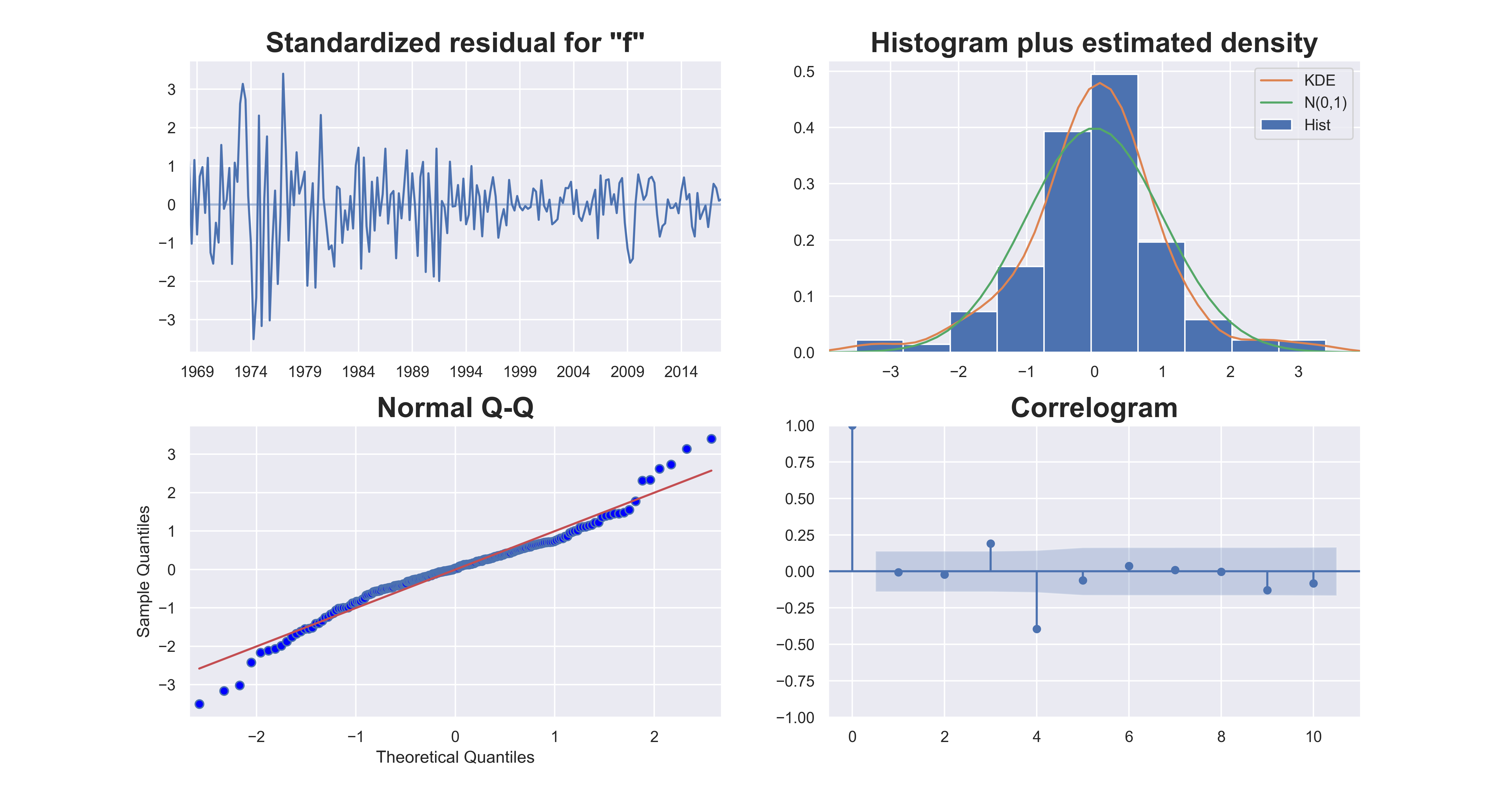

A more convenient way is to use the model.plot_diagnostics() method from statsmodels.

# better way to plot residual diagnostics

model.plot_diagnostics(figsize=(15,8))

plt.subplots_adjust(hspace=0.25)

standardized residual (top left): The residuals seem to fluctuate around a mean of zero but the variance does not look constant. In the period before 1080, the model tends to underpredict, resulting in larger residuals than later period. The residuals in 1990s and the period around and after 2012 are smaller than other time periods. This means that there may be structural changes in the data, and there are external factors should be accounted for, if possible.

Because of the patterns we see in the residual plot, we should run structural break tests on the data. But visually we can already tell there are structural breaks.

Histogram plus estimated density (top right): The standarized residual density is more concentrated in the middle, and does not look standard normal. But it is not too far deviated from it.

Normal Q-Q (bottom left): All the dots should fall perfectly in line with the red line. Any significant deviations would imply the distribution is skewed.

Correlogram (bottom right): The Correlogram, aka, ACF plot shows the residuals are autocorrelated at the 3rd lag (positive) and the 4th lag (negative). Any residual autocorrelation implies that there is some pattern in the data that are not explained by the model. We will need to find out if we can add more inputs and/or explain the discrepancy if we accept the limitation.

Model Evaluation 3: Out of Sample Testings

We have so far worked without any validation, which is certainly wrong. But we did that to focus on illustrating the individual pieces. When prediction/forecast is the goal, out of sample testing is essential for model performance evaluation.

One-Time Train/Test Split

Now, we will incorpate out of sample validation in model building.

from statsmodels.tsa.arima.model import ARIMA

# train/test

train = df.food[:200]

test = df.food[200:] # 14 records

model = ARIMA(train, order=(1, 1, 0)).fit()

# Forecast

fc= model.forecast(14, alpha=0.05) # 95% conf

forecast = model.get_forecast(14)

yhat = forecast.predicted_mean

yhat_conf_int = forecast.conf_int(alpha=0.05)

test_pred = test.to_frame().join([fc,yhat_conf_int])

title = "ARIMA Forecast (level)"

test_pred.plot()

plt.plot(train, label='training')

plt.fill_between(test.index, test_pred['lower food'], test_pred['upper food'],

color='k', alpha=.15)

plt.legend(frameon=False, loc='lower center', ncol=4)

# plot test data and forecast together with training data

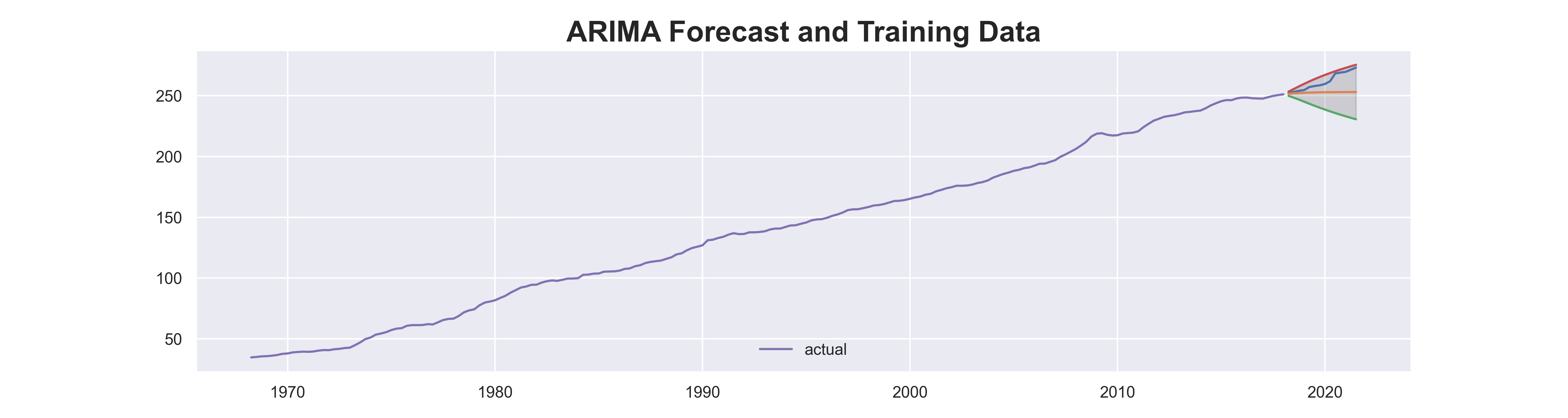

title ="ARIMA Forecast and Training Data"

plt.plot(test_pred)

plt.fill_between(test.index, test_pred['lower food'], test_pred['upper food'],

color='k', alpha=.15)

plt.plot(train,label='actual')

Using out-of-sample testing, we see that the forecast result is not good as it did not actually capture the upward trend. The actual food price is close to the 95% upper bound.

.png)

The forecast quality is bad.

Below is a snippet for the YoY out of sample testing.

# yoy

title = "ARIMA Forecast (yoy)"

train = df.food_yoy[:200]

test = df.food_yoy[200:]

model = ARIMA(train, order=(2, 1, 0)).fit()

# Forecast

fc= model.forecast(14, alpha=0.05) # 95% conf

forecast = model.get_forecast(14)

yhat = forecast.predicted_mean

yhat_conf_int = forecast.conf_int(alpha=0.05)

test_pred = test.to_frame().join([fc,yhat_conf_int])

test_pred.plot()

# plot test data and forecast together with training data

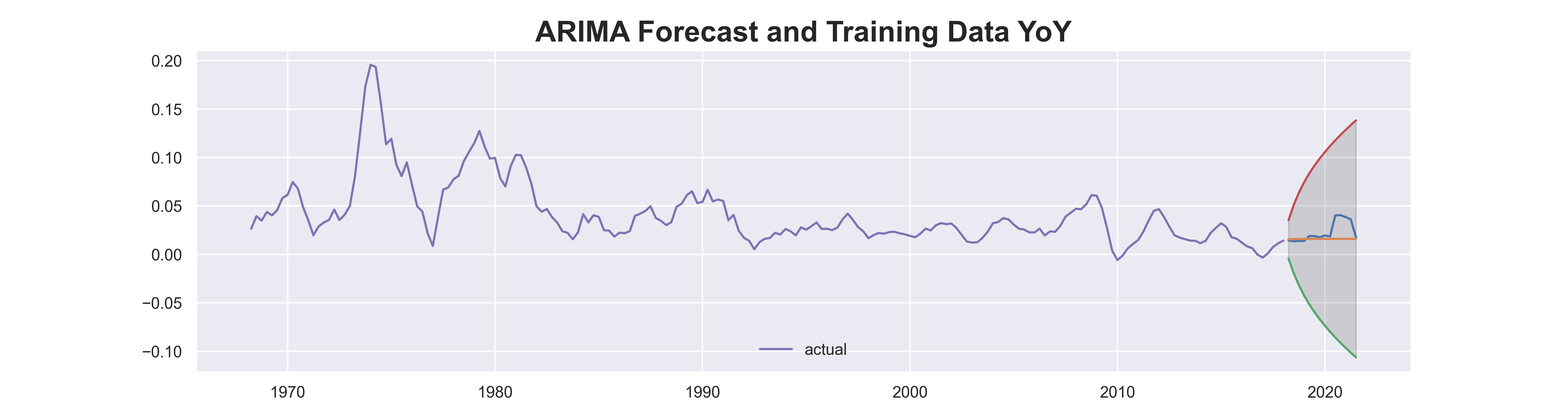

title ="ARIMA Forecast and Training Data YoY"

plt.plot(test_pred)

plt.fill_between(test.index, test_pred['lower food_yoy'], test_pred['upper food_yoy'],

color='k', alpha=.15)

plt.plot(train,label='actual')

plt.legend(frameon=False, loc='lower center', ncol=4)

accuracy_dict = accuracy_dict_function(test_pred.predicted_mean,test_pred.food_yoy)

accuracy_dict

[Out]:

{'mape': 0.26,

'me': -0.01,

'mae': 0.01,

'mpe': -0.19,

'rmse': 0.01,

'acf1': 0.67,

'adf_pvalue': 0.08,

'corr': 0.34}

We skip the first plot and look at the second plot with training data. The same problem with the level forecast shows in the YoY forecast as well. The forecasts completely misses the rising trend in the last few quarters. This is understandable, because our world just got shocked by Covid-19, which is completely an unexpected systematic stress that is not related to lags.

ARMA model is not suitable for stress testing.

Automatic ARIMA

It is not feasible for us to manually check each iteration for every model. So we will need an automated process for selecting the best model. See Tips to using auto_arima for the nuances for the hyper parameters.

There are two ways to run the automated procedure: stepwise and parallelized. The parallel approach is a naive, brute force grid search over all combinations of hyper parameters as specified. Because of its grid search nature, it can take longer time.

Here is from the documentation:

The auto-ARIMA process seeks to identify the most optimal parameters for an ARIMA model, settling on a single fitted ARIMA model. This process is based on the commonly-used R function,forecast::auto.arima.

Auto-ARIMA works by conducting differencing tests (i.e.,Kwiatkowski–Phillips–Schmidt–Shin, Augmented Dickey-Fuller orPhillips–Perron) to determine the order of differencing, d, and thenfitting models within ranges of defined start_p, max_p,start_q, max_q ranges. If the seasonal optional is enabled,auto-ARIMA also seeks to identify the optimal P and Q hyper-parameters after conducting the Canova-Hansen to determine the optimal order of seasonal differencing, D.

In order to find the best model, auto-ARIMA optimizes for a giveninformation_criterion, one of (‘aic’, ‘aicc’, ‘bic’, ‘hqic’, ‘oob’)(Akaike Information Criterion, Corrected Akaike Information Criterion,Bayesian Information Criterion, Hannan-Quinn Information Criterion, or”out of bag”–for validation scoring–respectively) and returns the ARIMAwhich minimizes the value.

Note that due to stationarity issues, auto-ARIMA might not find a suitable model that will converge. If this is the case, a ValueError will be thrown suggesting stationarity-inducing measures be taken priorto re-fitting or that a new range of order values be selected. Non-stepwise (i.e., essentially a grid search) selection can be slow,especially for seasonal data. Stepwise algorithm is outlined in Hyndman and Khandakar (2008)

model = pm.auto_arima(train.values, start_p=1, start_q=1,

test='adf', # use adftest to find optimal 'd'

max_p=3, max_q=3, # p=AR order, q = MA order)

m=1, # frequency of series

d=None, # let model determine number of differencing

seasonal=False, # No Seasonality

start_P=0,

D=0,

trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

model.summary()

Performing stepwise search to minimize aic

ARIMA(1,0,1)(0,0,0)[0] : AIC=-1272.709, Time=0.21 sec

ARIMA(0,0,0)(0,0,0)[0] : AIC=-606.610, Time=0.02 sec

ARIMA(1,0,0)(0,0,0)[0] : AIC=-1221.578, Time=0.02 sec

ARIMA(0,0,1)(0,0,0)[0] : AIC=-867.145, Time=0.08 sec

ARIMA(2,0,1)(0,0,0)[0] : AIC=-1264.990, Time=0.07 sec

ARIMA(1,0,2)(0,0,0)[0] : AIC=-1278.801, Time=0.25 sec

ARIMA(0,0,2)(0,0,0)[0] : AIC=-1021.603, Time=0.18 sec

ARIMA(2,0,2)(0,0,0)[0] : AIC=-1263.891, Time=0.12 sec

ARIMA(1,0,3)(0,0,0)[0] : AIC=-1337.314, Time=0.38 sec

ARIMA(0,0,3)(0,0,0)[0] : AIC=-1115.481, Time=0.23 sec

ARIMA(2,0,3)(0,0,0)[0] : AIC=-1327.319, Time=0.48 sec

ARIMA(1,0,3)(0,0,0)[0] intercept : AIC=-1348.572, Time=0.52 sec

ARIMA(0,0,3)(0,0,0)[0] intercept : AIC=inf, Time=0.60 sec

ARIMA(1,0,2)(0,0,0)[0] intercept : AIC=-1283.426, Time=0.43 sec

ARIMA(2,0,3)(0,0,0)[0] intercept : AIC=-1343.695, Time=0.58 sec

ARIMA(0,0,2)(0,0,0)[0] intercept : AIC=-1145.968, Time=0.38 sec

ARIMA(2,0,2)(0,0,0)[0] intercept : AIC=-1274.859, Time=0.53 sec

Best model: ARIMA(1,0,3)(0,0,0)[0] intercept

Total fit time: 5.116 seconds

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 200

Model: SARIMAX(1, 0, 3) Log Likelihood 680.286

Date: Wed, 19 May 2021 AIC -1348.572

Time: 10:25:43 BIC -1328.782

Sample: 0 HQIC -1340.563

- 200

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

intercept 0.0148 0.004 3.630 0.000 0.007 0.023

ar.L1 0.6647 0.047 14.212 0.000 0.573 0.756

ma.L1 0.8489 0.053 16.156 0.000 0.746 0.952

ma.L2 0.8115 0.049 16.617 0.000 0.716 0.907

ma.L3 0.8911 0.054 16.511 0.000 0.785 0.997

sigma2 6.738e-05 5.7e-06 11.817 0.000 5.62e-05 7.86e-05

===================================================================================

Ljung-Box (L1) (Q): 0.26 Jarque-Bera (JB): 108.74

Prob(Q): 0.61 Prob(JB): 0.00

Heteroskedasticity (H): 0.14 Skew: 1.06

Prob(H) (two-sided): 0.00 Kurtosis: 5.92

===================================================================================

The automated procedure shows that ARIMA(1,0,3) is the best model, with 1 lag and 3 MA terms.

Using Auto-ARIMA to Forecast

Fit an ARIMA to a vector, y, of observations with an optional matrix of exogenous variables, and then generate predictions.

Parameters

y : The time-series to which to fit the ARIMA estimator. This mayeither be a Pandas Series object or a numpy array. This should be a one-dimensional array of floats, and should not contain anynp.nan or np.inf values.

X : An optional 2-d array of exogenous variables. If provided, these variables are used as additional features in the regression operation. This should not include a constant or trend.

n_periods : (default=10) The number of periods in the future to forecast.

Automated ARIMA

import pmdarima as pm

model = pm.auto_arima(train.values, start_p=1, start_q=1,

test='adf', # use adftest to find optimal 'd'

max_p=3, max_q=3, # maximum p and q

m=4, # frequency of series, period for seasonal differencing

d=None, # let model determine 'd'

seasonal=False, # No Seasonality

start_P=0,

D=0,

trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

model.summary()

pred = model.fit_predict(train, n_periods=len(test))

pred_s = pd.Series(pred, index=test.index)

pred_s.name='pred'

test.to_frame().join(pred_s).plot()

# Forecast

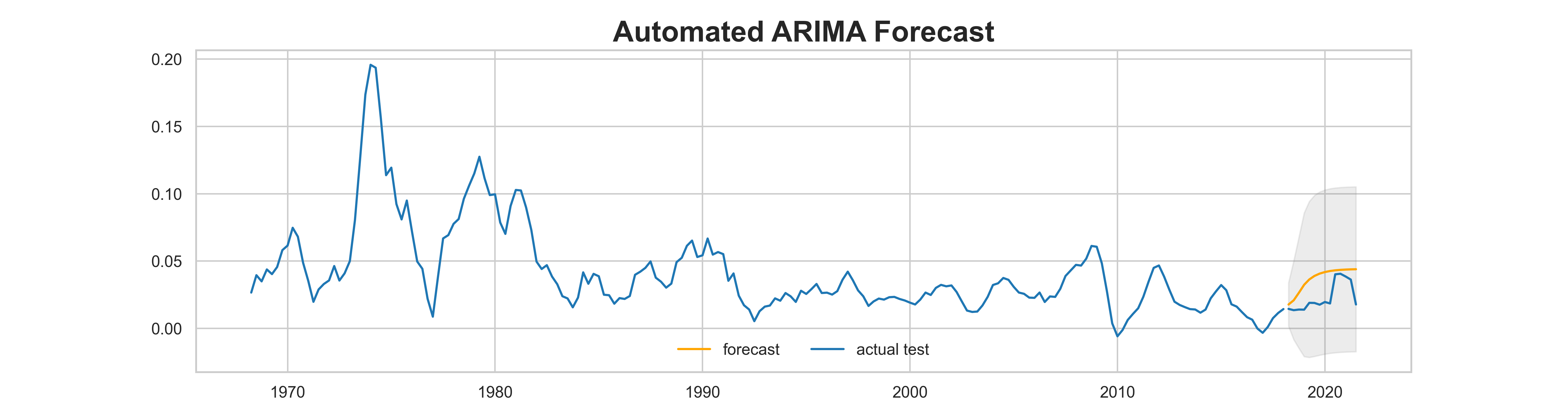

title = "Automated ARIMA Forecast"

n_periods = len(test)

fc, confint = model.fit_predict(train, n_periods=n_periods, return_conf_int=True) # train is 1 dim

fc_idx = test.index

# for plotting

fc_series = pd.Series(fc, index=fc_idx)

low = pd.Series(confint[:, 0], index=fc_idx)

high = pd.Series(confint[:, 1], index=fc_idx)

# Plot

sns.set_style('white')

plt.plot(train, color=blue)

plt.plot(fc_series, color='orange', label='forecast')

plt.plot(test, color=blue, label='actual test')

plt.fill_between(low.index,

low,

high,

color='grey', alpha=.15)

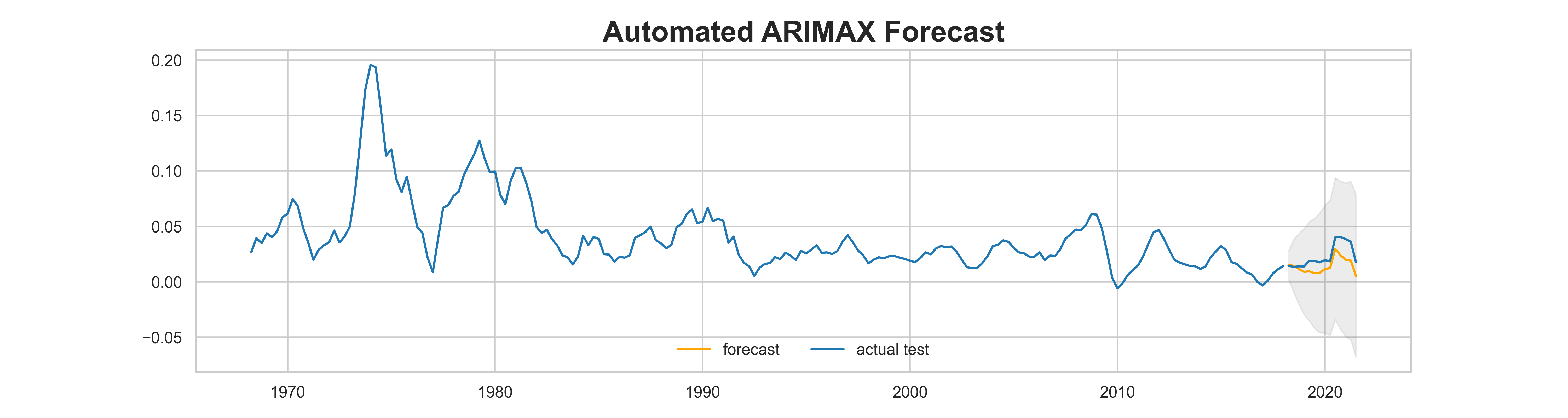

The result looks better than the one manually created.

ARIMAX with X (exogenous)

Let’s pretend that meat prices drive food prices. The downside is that in order to make predictions for food_yoy, we will need the forecast for meat_yoy.

import pmdarima as pm

# train, X=df.meat_yoy[:200].to_frame() will also work, as long as they have the same index

model = pm.auto_arima(train.values, X=df.meat_yoy[:200].values.reshape(-1,1) ,start_p=1, start_q=1,

test='adf', # use adftest to find optimal 'd'

max_p=3, max_q=3, # maximum p and q

m=4, # frequency of series, period for seasonal differencing

d=None, # let model determine 'd'

seasonal=False, # No Seasonality

start_P=0,

D=0,

trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

[Out]:

Performing stepwise search to minimize aic

ARIMA(1,0,1)(0,0,0)[0] : AIC=-1406.458, Time=0.42 sec

ARIMA(0,0,0)(0,0,0)[0] : AIC=-799.668, Time=0.05 sec

ARIMA(1,0,0)(0,0,0)[0] : AIC=-1365.289, Time=0.16 sec

ARIMA(0,0,1)(0,0,0)[0] : AIC=-1032.365, Time=0.11 sec

ARIMA(2,0,1)(0,0,0)[0] : AIC=-1422.762, Time=0.37 sec

ARIMA(2,0,0)(0,0,0)[0] : AIC=-1420.931, Time=0.29 sec

ARIMA(3,0,1)(0,0,0)[0] : AIC=-1427.298, Time=0.48 sec

ARIMA(3,0,0)(0,0,0)[0] : AIC=-1422.412, Time=0.39 sec

ARIMA(3,0,2)(0,0,0)[0] : AIC=-1409.680, Time=0.73 sec

ARIMA(2,0,2)(0,0,0)[0] : AIC=-1425.466, Time=0.37 sec

ARIMA(3,0,1)(0,0,0)[0] intercept : AIC=-1424.524, Time=0.57 sec

Best model: ARIMA(3,0,1)(0,0,0)[0]

model.summary()

[Out]:

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 200

Model: SARIMAX(3, 0, 1) Log Likelihood 719.649

Date: Wed, 19 May 2021 AIC -1427.298

Time: 17:59:28 BIC -1407.508

Sample: 0 HQIC -1419.289

- 200

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.2302 0.011 21.677 0.000 0.209 0.251

ar.L1 0.6662 0.085 7.817 0.000 0.499 0.833

ar.L2 0.5983 0.126 4.732 0.000 0.350 0.846

ar.L3 -0.2915 0.066 -4.398 0.000 -0.421 -0.162

ma.L1 0.9110 0.055 16.435 0.000 0.802 1.020

sigma2 4.259e-05 3.55e-06 12.005 0.000 3.56e-05 4.95e-05

===================================================================================

Ljung-Box (L1) (Q): 1.26 Jarque-Bera (JB): 32.33

Prob(Q): 0.26 Prob(JB): 0.00

Heteroskedasticity (H): 0.17 Skew: -0.01

Prob(H) (two-sided): 0.00 Kurtosis: 4.97

# model.predict(n_periods=10, X=None, return_conf_int=False, alpha=0.05, **kwargs)

pred = model.predict(n_periods=14, X=df.meat_yoy[200:].to_frame())

pred_s = pd.Series(pred, index=test.index)

pred_s.name='pred'

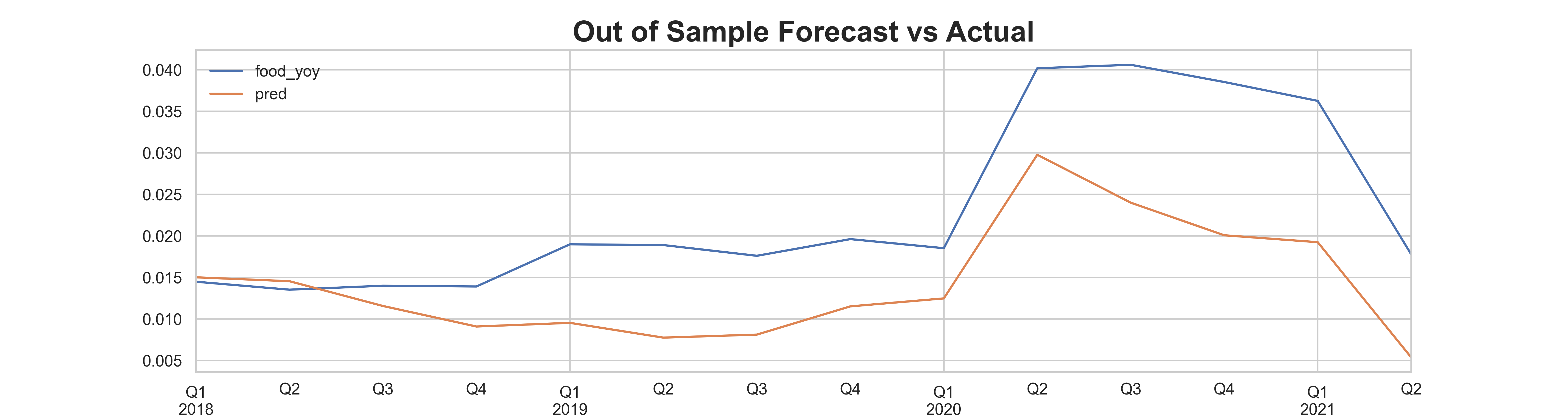

title = "Out of Sample Forecast vs Actual"

test.to_frame().join(pred_s).plot()

We see that the result is a lot better. This is because we have the actual meat data for the forecast period. This is in fact “cheating”. Because in reality, we do not know what meat prices are in the future. We will need to develope a model to forecast meat prices before using the ARIMAX model.

title = "Automated ARIMAX Forecast"

n_periods = len(test)

fc, confint = fc, confint = model.predict(n_periods=n_periods,

exogenous=df.meat_yoy[200:].to_frame(),

return_conf_int=True)

fc_idx = test.index

fc_series = pd.Series(fc, index=fc_idx)

low = pd.Series(confint[:, 0], index=fc_idx)

high = pd.Series(confint[:, 1], index=fc_idx)

# Plot

sns.set_style('whitegrid')

plt.plot(train, color=blue)

plt.plot(fc_series, color='orange', label='forecast')

plt.plot(test, color=blue, label='actual test')

plt.fill_between(low.index,

low,

high,

color='grey', alpha=.15)

Model Evaluation: Walk Forward Expanding Window Train Test

The purpose of out of sample test/validation is to evaluate model specification and the robustness in predictions. There are different schemes for splitting up the time-indexed data for train and test.

n_train = 195

n_records = df.shape[0]

accuracy_lt =[]

for i in range(n_train, n_records-14):

train, test = df.food_yoy[0:i], df.food_yoy[i:i+14]

# print('train=%d, test=%d' % (len(train), len(test)))

exogenous_train = df.meat_yoy[0:i].to_frame()

exogenous_test = df.meat_yoy[i:i+14].to_frame()

# print("test", test.shape)

# print("exogenous_train",exogenous_train.shape)

# print("exogenous_test",exogenous_test.shape)

# print("train", train.shape)

axmodel = pm.auto_arima(train, exogenous=exogenous_train,

start_p=1, start_q=1,

test='adf',

max_p=3, max_q=3, m=12,

start_P=0, seasonal=False,

d=None, D=1, trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

print("i = ", i)

print(axmodel.summary())

fc, conf_int = model.predict(n_periods=14, X = exogenous_test, return_conf_int=True, alpha=0.05)

fc_s = pd.Series(fc, index=test.index)

fc_s.name='fc'

conf_int_df = pd.DataFrame(conf_int, index=test.index, columns=['lower food_yoy','upper food_yoy' ])

test_pred = test.to_frame().join([fc_s,conf_int_df])

accuracy_dict = accuracy_dict_function(test_pred.fc,test_pred.food_yoy)

# test_pred.plot()

# plt.fill_between(test.index, test_pred['lower food_yoy'], test_pred['upper food_yoy'],

# color='k', alpha=.15)

# plt.legend(frameon=False, loc='lower center', ncol=4)

# plt.show()

accuracy_lt.append(accuracy_dict)

accuracy_df = pd.DataFrame(accuracy_lt)

accuracy_df

[Out]:

# mape me mae mpe rmse acf1 adf_pvalue corr

# 0 0.350 -0.000 0.000 -0.220 0.010 0.810 0.990 0.740

# 1 0.400 -0.010 0.010 -0.180 0.010 0.700 1.000 0.840

# 2 0.310 -0.010 0.010 -0.300 0.010 0.670 0.940 0.850

# 3 0.310 -0.010 0.010 -0.300 0.010 0.710 0.130 0.830

# 4 0.340 -0.010 0.010 -0.320 0.010 0.750 0.000 0.830