- Bonds vs. Dividend Stocks

- Types of Muni Bonds

- Who invest in munis

- Historical perspectives

- Current situation and outlook

- Risks in Munis

- Muni bond insurance

- Climate risk in Muni bonds

- Interest rate sensitivities

- Compute bond price

- Convexity

- Reference

Bonds vs. Dividend Stocks

Dividend stocks and bonds are two different types of investments that serve different purposes in an investor’s portfolio.

- Dividend Stocks:

- Dividend stocks are shares of companies that distribute a portion of their earnings to shareholders in the form of dividends. These dividends are typically paid regularly, such as quarterly or annually.

- Investing in dividend stocks can provide investors with a steady stream of income, making them particularly attractive for income-oriented investors, such as retirees.

- Dividend stocks also offer the potential for capital appreciation, as the stock price may increase over time, providing additional returns beyond the dividends.

- However, dividend stocks are typically more volatile than bonds, as their value is influenced by factors such as company performance, market conditions, and investor sentiment.

- Bonds:

- Bonds are debt securities issued by governments, municipalities, or corporations to raise capital. When an investor buys a bond, they are essentially lending money to the issuer in exchange for regular interest payments and the return of the principal amount at maturity.

- Bonds are generally considered less risky than stocks because they provide a fixed income stream and have a defined maturity date when the principal is repaid.

- Depending on the type of bond, they can offer different levels of risk and return. For example, government bonds are typically considered safer than corporate bonds, but they may offer lower returns.

- Bonds can also provide diversification benefits to a portfolio, as they often have low correlation with stocks and other asset classes.

In summary, dividend stocks are equity investments that offer the potential for income and capital appreciation but come with higher volatility, while bonds are debt investments that provide a fixed income stream and are generally less risky but offer lower potential returns. Investors often hold a mix of both dividend stocks and bonds in their portfolios to achieve a balance between income, growth, and risk.

| Compare | Dividend Stocks | Muni Bonds |

|---|---|---|

| Periodic stable “rental” income | Maybe | yes |

| Possible capital appreciation | Yes | No |

| Risk | more volatile; high | low |

| Energy and time required from investor | A lot | not much |

| Suitable to | Not limited | high net worth people seeking capital preservation; institutions seeking diversification |

Types of Muni Bonds

Municipal bonds, or “munis,” are debt securities issued by state or local governments, municipalities, or their agencies to finance public projects such as roads, schools, hospitals, and infrastructure development. Their credit quality can vary significantly depending on the financial health of the issuing municipality. Investors should conduct thorough research or consult with a financial advisor to assess the creditworthiness of municipal bond issuers before investing.

There are 2 types of municipal bonds:

- GO (general obligation) bonds (backed by the full faith and credit of the issuer),

- revenue bonds (backed by specific revenue streams, such as tolls or utility payments)

In addition, municipalities may borrow short term. Those debt securities are called “municipal notes”.

Who invest in munis

Municipal bonds are a possible place to get steady income streams for investors seeking, as the interest income generated from these bonds is often exempt from federal income taxes and, in some cases, state and local taxes, particularly if the investor resides in the same state as the issuer. This tax advantage can make munis attractive to investors in the highest tax brackets.

Historical perspectives

Historically, muni bonds are among the safest investoments. Whether it will remain so depends on the underlying conditions will remain true for the future.

Municipal debt predates corporate debt by several centuries—the early Renaissance Italian city-states borrowed money from major banking families. Borrowing by American cities dates to the nineteenth century, and records of U.S. municipal bonds indicate use around the early 1800s. Officially the first recorded municipal bond was a general obligation bond issued by the City of New York for a canal in 1812.

The American Civil War (April 12, 1861 – May 26, 1865)

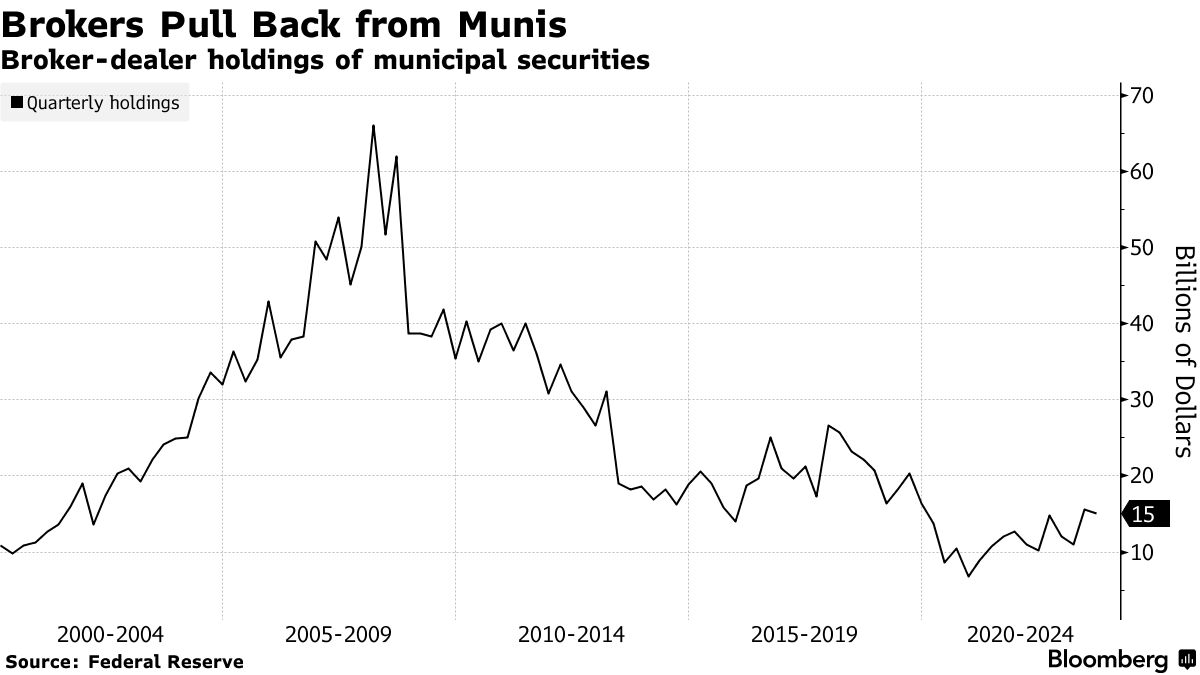

Current situation and outlook

Citigroup exit muni bonds market. According to Citi, underwriting state and local debt was too big a drag on the bottom line, unable to compete with more lucrative lines of work. UBS Group AG made a similar decision in October, 2023.

Bloomberg Citigroup’s Muni-Market Exit Sows Fears of a Wall Street Retreat

- More costly for local governments to finance infrastructure

- Potential increase in liquidity risk as broker dealers have already reduced their holdings of state and local government bonds sharply since the 2008 credit crisis.

Even though it’s exiting the underwriting business, Citigroup will still be a buyer of municipal bonds, like other banks who invest in the securities. The Wall Street giant holds nearly $10 billion of state and municipal debt securities, according to regulatory filings. The vast majority of that is classified as held-to-maturity.

Risks in Munis

Munis are relatively low risk. But there are still defaults, such as Detroit and Puerto Rico.

Bond market values are inversely related to interest rates. If interest rates go higher, bond market value are reduced due to discounting. For example, say we bought a muni bond that pays 3%. Now the interest rate increases to 10%, we not only have the opportunity cost of “could have gotten 10% instead of 3%”, but also if we were to sell the bond, we would have to sell it at a lower price…because who wants to get 3% instead of 10%.

Price Risk: If interest rates rise during the term of your bond, you’re losing out on a better rate. This will also cause the bond you are holding to decline in value. Default Risk: Issuer defaults.

The longer the term of the bond, the greater these risks are. We can evaluate muni risks from 3 perspectives:

- issuer’s financial health (obligor credit rating)

- global, national, and local economic conditions: population growth rate, GDP growth rate per capita, unemployment rate, etc.

- specific features of the bond itself

Using Puerto Rico as an example:

Financial health: To pay evergrowing deficit, it borrowed. Over a decade, 18 different government entities borrowed many muni debt: muni bonds were issued to pay for schools, stadiums, hospitals, salaries, old debt, pensions, and more. The island has no cental office overseeing bond-proceed spending. No one knows exactly where the money went (wow! Isn’t that corruption or poor governance?)

Economy: Since 2006, Puerto Rico’s economy contracted every year but one.

Specific features of the bond itself: the interest income is exempt from local, state, and federal taxes everywhere in the US (very special treatment!) & Wall Streeet was eager to lend.

- Creditworthiness of the Issuer:

- budgetary practices,

- debt levels

- revenue sources, and overall economic health. Credit rating agencies such as Moody’s, Standard & Poor’s, and Fitch provide credit ratings for municipal bonds, which can serve as a starting point for evaluating credit risk.

Bonds with a rating of BBB- (on the Standard & Poor’s and Fitch scale) or Baa3 (Moody’s) or better are considered “investment-grade.” Bonds with lower ratings are considered “speculative” and often referred to as “high-yield” or “junk” bonds.

-

Revenue Source: Determine the revenue source backing the bonds. General obligation bonds are typically backed by the full faith and credit of the issuer, while revenue bonds are backed by specific revenue streams (e.g., tolls, utility payments). Assess the stability and predictability of the revenue source, as well as any potential risks that could impact revenue generation.

-

Debt Structure: Evaluate the debt structure of the bonds, including maturity dates, interest rates, and call provisions. Longer maturity bonds may be more susceptible to interest rate risk, while callable bonds carry the risk of early redemption by the issuer. Understanding these features can help assess the bond’s sensitivity to changes in interest rates and potential early repayment risk.

-

Market Conditions: Consider prevailing market conditions, including interest rate trends, credit spreads, and liquidity conditions. Changes in interest rates can impact bond prices, while liquidity conditions can affect the ease of buying or selling bonds in the secondary market.

-

Legal and Regulatory Risks: Understand any legal or regulatory risks associated with the bonds, such as changes in tax laws or regulations affecting municipal finance. Keep abreast of legislative developments and legal challenges that could impact the issuer’s ability to meet its obligations.

-

Issuer-Specific Risks: Evaluate any issuer-specific risks, such as exposure to specific industries or sectors, political instability, or governance issues. Assess how these factors may affect the issuer’s ability to repay bondholders.

-

Tax Considerations: Consider the tax implications of investing in municipal bonds, including the potential tax-exempt status of interest income at the federal, state, and local levels. Understand how changes in tax laws or regulations could impact the after-tax return on investment.

-

Diversification: Spread investment across multiple municipal bonds or bond issuers to mitigate concentration risk. Diversification can help reduce the impact of credit events or defaults on individual bonds.

By conducting thorough due diligence and considering these factors, investors can better evaluate the risks associated with investing in municipal bonds and make informed investment decisions. It’s also advisable to consult with a financial advisor or investment professional for personalized guidance tailored to your specific financial situation and investment objectives.

Muni bond insurance

Higher interest rates increase the attractiveness of bond insurance, while also allowing for higher investment income from the fixed income portfolio.

Climate risk in Muni bonds

Because muni bonds are long term debt.

U.S. Senator Sheldon Whitehouse (D-RI), Chairman of the U.S. Senate Budget Committee,“Investing in the Future: Safeguarding Municipal Bonds from Climate Risk.” Which brings us to the topic of today’s hearing: the $4 trillion municipal bond market.

Municipal bonds—much like the 30-year mortgage—are a bedrock of our American economic system, enabling local governments to make investments that are essential for their communities: basic public services like water service, sewage treatment, electricity, and roads. Local government bonds finance more than 70 percent of U.S. infrastructure, including airports, bridges, railways, and seaports. Climate change now threatens that bond market.

Historically, municipal bonds have a sterling reputation among investors, with default rates of less than one percent. Investors lend their dollars to build a new school or highway and typically receive a tax-exempt stream of interest for the next fifteen or even thirty years. These bonds, secured by government revenues, are among our most stable investments.

Climate change undermines this stability in two ways. More intense storms, wildfires, droughts, heatwaves, and floods impose higher costs on state and local governments, putting pressure on the spending side. And on the revenue side, storm damage and insurance risk can undermine the municipal tax base. Already, climate change is making it harder for municipalities to service their bond payments and making it harder for governments to raise new capital for needed climate investments.

After a disaster, communities’ local tax bases can be devastated. Five years after the Camp Wildfire, only a third of the population has returned to Paradise, California. Hurricane Matthew undermined tax bases across small towns in North Carolina. After a disaster, population declines mean revenues decline.

And bond markets are watching; fifteen- or thirty-year municipal bonds start to look less safe. Moody’s has already given notice to coastal communities.

This risk comes home to roost in the federal budget. Over 40 percent of our national debt relates back to crises we did not prepare for, like the mortgage meltdown and the covid pandemic. Today, we’ll hear more evidence that climate change is just such a crisis—an “impending budgetary and fiscal crisis facing our nation.” It could well be the worst yet. We’ve heard warnings about a coastal property values crash, a similar collapse in wildfire-adjacent areas, a bursting of the “carbon bubble,” of turmoil in insurance markets, climate inflation, and now danger to a pillar of American investment. Nothing says this all doesn’t come to pass. Ignoring it is akin to financial negligence. If there’s one thing we should be able to agree on, it’s that we can’t afford to be negligent.

Interest rate sensitivities

Bond prices are very sensititve to interest rates. When evaluating the interest rate sensitivity of municipal bonds, several measures are commonly used. These measures help investors understand how changes in interest rates affect bond prices. The main measures include duration, convexity, and modified duration. Let’s briefly discuss each:

-

Duration: Duration is a measure of the sensitivity of a bond’s price to changes in interest rates. It represents the weighted average time to receive the bond’s cash flows, taking into account both the coupon payments and the return of the bond’s face value at maturity. Duration provides an estimate of the percentage change in the bond’s price for a 1% change in interest rates.

-

Modified Duration: Modified duration is a modified version of duration that accounts for the fact that bond prices and yields move in opposite directions. It’s calculated by dividing the bond’s duration by (1 + yield), where yield is expressed as a decimal. Modified duration provides an estimate of the percentage change in the bond’s price for a 1% change in yield.

-

Convexity: Convexity is a measure of the curvature of the bond’s price-yield relationship. It provides additional information beyond duration by capturing the second-order effect of changes in interest rates on bond prices. Convexity measures how much a bond’s duration changes as interest rates change. It helps refine the estimate provided by duration, especially for larger interest rate changes.

-

Yield to Maturity (YTM): Yield to maturity represents the total return an investor can expect to receive by holding the bond until maturity, taking into account its current market price, coupon payments, and face value. YTM is also used as a measure of interest rate sensitivity because it reflects the relationship between the bond’s current price and its coupon payments.

These measures are essential tools for bond investors to assess and manage interest rate risk in their portfolios. Duration and convexity are particularly useful for estimating the impact of interest rate changes on bond prices, while modified duration and yield to maturity provide additional insights into the bond’s sensitivity to interest rate movements.

Compute bond price

Sure, here’s a simple Python code snippet to calculate the price of a bond:

def calculate_bond_price(face_value, coupon_rate, yield_to_maturity, years_to_maturity):

"""

Calculate the price of a bond.

Args:

face_value (float): Face value of the bond.

coupon_rate (float): Annual coupon rate (as a percentage).

yield_to_maturity (float): Yield to maturity (as a percentage).

years_to_maturity (int): Years to maturity of the bond.

Returns:

float: Price of the bond.

"""

coupon_payment = face_value * coupon_rate / 100

present_value = 0

for t in range(1, years_to_maturity + 1):

present_value += coupon_payment / (1 + yield_to_maturity / 100) ** t

present_value += face_value / (1 + yield_to_maturity / 100) ** years_to_maturity

return present_value

# Example usage

face_value = 1000 # Face value of the bond

coupon_rate = 5 # Annual coupon rate (as a percentage)

yield_to_maturity = 4 # Yield to maturity (as a percentage)

years_to_maturity = 5 # Years to maturity of the bond

bond_price = calculate_bond_price(face_value, coupon_rate, yield_to_maturity, years_to_maturity)

print("Bond price:", round(bond_price, 2))

This code defines a function calculate_bond_price that takes the face value, coupon rate, yield to maturity, and years to maturity of a bond as input and returns the price of the bond. The price is calculated by discounting the future cash flows (coupon payments and face value at maturity) back to their present value using the yield to maturity.

You can adjust the values of face_value, coupon_rate, yield_to_maturity, and years_to_maturity to calculate the price of different bonds.

Bond duration

Municipal bond duration is a measure of the sensitivity of a municipal bond’s price to changes in interest rates. It helps investors understand the potential impact of interest rate changes on the bond’s value. Duration is expressed in years and provides an estimate of the bond’s price volatility.

Here’s a Python code snippet to calculate the duration of a municipal bond:

def calculate_muni_bond_duration(face_value, coupon_rate, yield_to_maturity, years_to_maturity):

"""

Calculate the duration of a municipal bond.

Args:

face_value (float): Face value of the bond.

coupon_rate (float): Annual coupon rate (as a percentage).

yield_to_maturity (float): Yield to maturity (as a percentage).

years_to_maturity (int): Years to maturity of the bond.

Returns:

float: Duration of the bond.

"""

coupon_payment = face_value * coupon_rate / 100

present_value = 0

for t in range(1, years_to_maturity + 1):

present_value += (coupon_payment / (1 + yield_to_maturity / 100) ** t) * t

present_value += (face_value / (1 + yield_to_maturity / 100) ** years_to_maturity) * years_to_maturity

bond_price = present_value / (1 + yield_to_maturity / 100)

macaulay_duration = present_value / bond_price

return macaulay_duration

# Example usage

face_value = 1000 # Face value of the bond

coupon_rate = 5 # Annual coupon rate (as a percentage)

yield_to_maturity = 4 # Yield to maturity (as a percentage)

years_to_maturity = 5 # Years to maturity of the bond

bond_duration = calculate_muni_bond_duration(face_value, coupon_rate, yield_to_maturity, years_to_maturity)

print("Municipal bond duration:", round(bond_duration, 2), "years")

Convexity

Convexity is another important measure used in bond analysis, especially when assessing the sensitivity of bond prices to changes in interest rates. It provides additional information beyond duration by accounting for the curvature of the price-yield relationship. Here’s a Python code snippet to calculate the convexity of a municipal bond:

def calculate_muni_bond_convexity(face_value, coupon_rate, yield_to_maturity, years_to_maturity):

"""

Calculate the convexity of a municipal bond.

Args:

face_value (float): Face value of the bond.

coupon_rate (float): Annual coupon rate (as a percentage).

yield_to_maturity (float): Yield to maturity (as a percentage).

years_to_maturity (int): Years to maturity of the bond.

Returns:

float: Convexity of the bond.

"""

coupon_payment = face_value * coupon_rate / 100

present_value = 0

for t in range(1, years_to_maturity + 1):

present_value += (coupon_payment / (1 + yield_to_maturity / 100) ** t) * (t ** 2 + t)

present_value += (face_value / (1 + yield_to_maturity / 100) ** years_to_maturity) * (years_to_maturity ** 2 + years_to_maturity)

bond_price = present_value / (1 + yield_to_maturity / 100)

convexity = present_value / (bond_price * (1 + yield_to_maturity / 100) ** 2)

return convexity

# Example usage

face_value = 1000 # Face value of the bond

coupon_rate = 5 # Annual coupon rate (as a percentage)

yield_to_maturity = 4 # Yield to maturity (as a percentage)

years_to_maturity = 5 # Years to maturity of the bond

bond_convexity = calculate_muni_bond_convexity(face_value, coupon_rate, yield_to_maturity, years_to_maturity)

print("Municipal bond convexity:", round(bond_convexity, 2))

This code calculates the convexity of a municipal bond. Convexity measures the curvature of the bond’s price-yield relationship. It’s calculated as the second derivative of the bond price formula with respect to yield, divided by the bond price.

The function calculate_muni_bond_convexity takes the face value, coupon rate, yield to maturity, and years to maturity of the bond as input and returns the convexity of the bond.

You can adjust the values of face_value, coupon_rate, yield_to_maturity, and years_to_maturity to calculate the convexity of different municipal bonds.

Reference

Schwab: potential opportunities muni bond market WHITEHOUSE: Climate change is threatening the municipal bond market

Bond Savvy, Steve Shaw, Eight Reasons Not To Own Vanguard VMFXX Bond Savvy, Steve Shaw, Corporate Bonds vs. Municipal Bonds