- Accounting classifications of bank assets

- Why do banks own securities besides loans

- Reclassifying

- Unanswered questions

- Reference

Accounting is a complicated topic. This post tries to summarize the types of accounting classifications on bank assets and impacts on reclassification.

Images of this post are from New York Fed Quarterly Trends for Consolidated U.S. Banking Organizations, based on onsolidated financial statistics for the U.S. commercial banking industry, including both bank holding companies (BHCs) and banks. Statistics are based on quarterly regulatory filings. Statistics are inclusive of BHCs’ nonbank subsidiaries.

Accounting classifications of bank assets

Below is a summary of the three accounting classifications of bank assets:

Trading: Securities (debt and equity) that are bought and held for the purpose of selling in the near term. They are reported at fair value. Unrealized gains and losses are included in the earnings. Trading book is always marked to market.

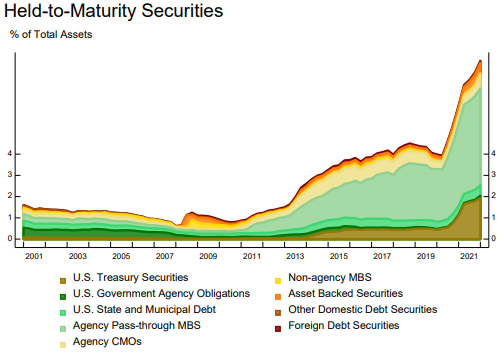

Held to maturity (HTM): Debt securities (bonds) that the firm has the positive intent and ability to hold until maturity. (Equities can’t be included in this category since they don’t mature.) The debt securities are reported at amortized cost. Note that SVB held most of their investments in long term governament bond. They had big paper losses due to rising interest rates. But these unrealized losses were not impacting their earnings if they were not forced to take losses until tide changed. Their start-up founder customers were in need of their money and wanted to take money out. So SVB tried to sell the bonds in a time of rising interest rate and the losses piled on until a bank run happened…and the bank run was rapid due to panic as most of the deposits were over the FDIC limits.

Bank of America had $132 billion of unrealized losses in its held-to-maturity portfolio at the end of September, 2023, made up of government bonds and mortgage-related securities guaranteed by official agencies. Banks’ hidden losses are surprise survivor of 2023

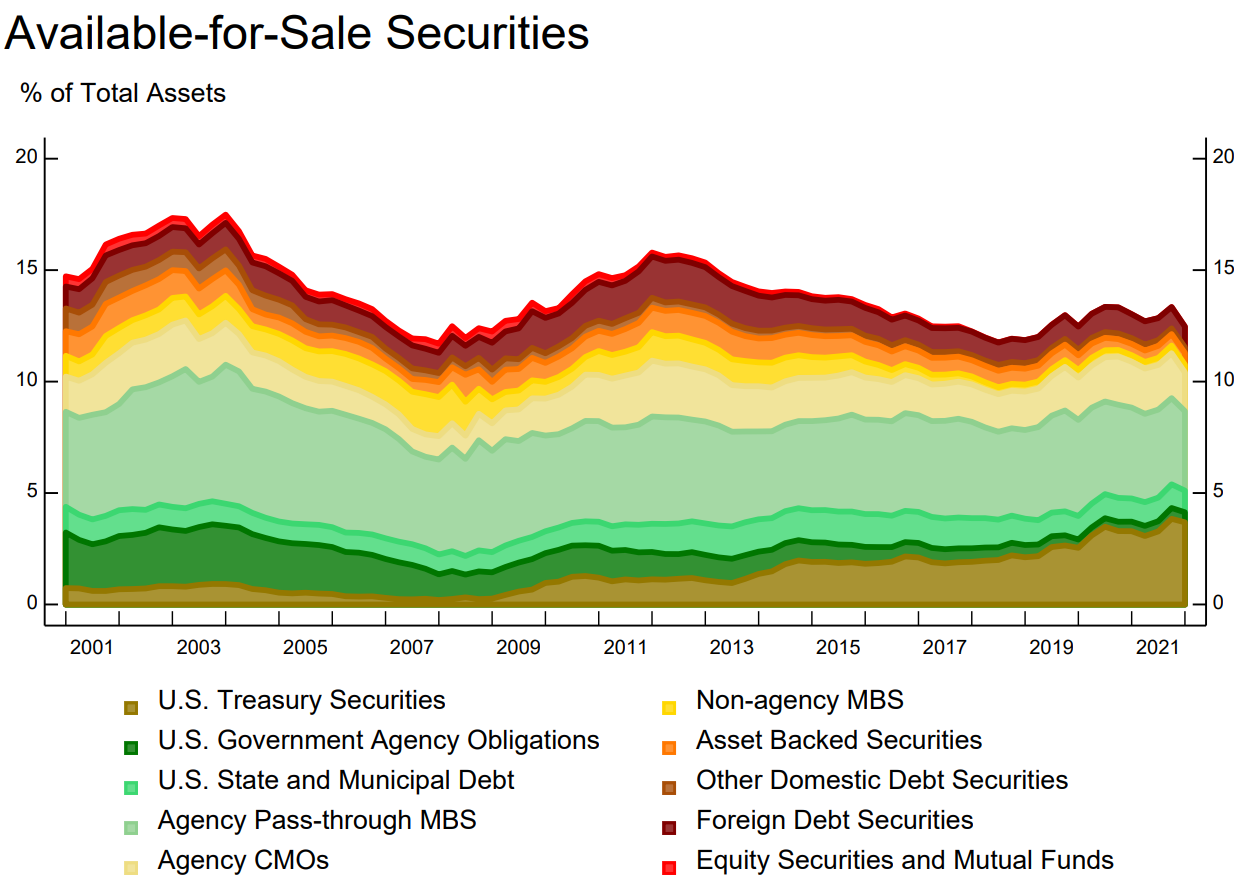

Available for sale (AFS): A catch-all for debt and equity securities not captured by either of the above definitions. These are securities that the bank may retain for long periods but that may also be sold. Often, they are held in the Treasury department of large banks. The types of securities may include: US Treasury, sovereign debt, MBS, municipal bonds, corporate bonds, and so on. They are reported at fair value. However, non-credit related unrealized gains and losses are excluded from earnings. The noncredit-related component of the fair value decline is recognized in other comprehensive income (OCI). See source. However, OCI does impact regulatory capital per Basel III.

Because of the different accounting treatments, in particular on HTM and AFS, banks have been reclassifying their assets for various purposes.

Why do banks own securities besides loans

To understand how and why banks classify assets, we should first know why banks hold security assets in addition to loans.

-

Banks may face an imbalance between desposits and lendings. For example, there may not be enough good profitable lending opportunities. In such cases, funding-rich banks may choose to invest in securities that reflect lending by other banks or by nonbank lenders (e.g., mortgage-backed securities issued by another lender), or direct debt issuance by nonfinancial firms (e.g., corporate bonds).

-

For risk management and to meet regulatory requirements: securities can be sold more easily and with lower price impact than loans, for which the secondary market is less active. Regulation such as the liquidity coverage ratio developed as part of the Basel III Capital Accord requires banks to hold enough high-quality liquid assets to meet their liquidity needs under a thirty-day liquidity stress scenario.

-

From a risk management point of view, holding securities may help the bank diversify or mitigate its risk exposures. Conversely, adjusting securities holdings can provide a straightforward way for banks to ramp up their level of risk in an effort to increase expected returns. For example, recent research argues that banks respond to expansionary monetary policy by lengthening the maturity of their securities portfolios, in an effort to boost yields.

-

Keeping an inventory of securitiesfor market-making, broker-dealers services.

-

Regulatory arbitrage: holding securities instead of loans may reduce capital requirements.

Why banks own bonds in their asset

Banks hold bonds in their assets for several reasons, including:

-

Diversification of Assets: Holding a variety of assets, including bonds, helps banks diversify their investment portfolios. Bonds provide a relatively stable source of income compared to other assets like stocks, which can be more volatile. By diversifying their assets, banks can reduce their overall risk exposure.

-

Liquidity Management: Bonds can serve as a source of liquidity for banks. Banks can easily buy and sell bonds in the secondary market to manage their short-term liquidity needs. This flexibility is particularly important for banks to meet unexpected withdrawals or funding requirements.

-

Interest Income: Bonds generate interest income for banks. When banks purchase bonds, they receive periodic interest payments from the bond issuer. This interest income contributes to the bank’s overall revenue stream and helps support profitability.

-

Regulatory Requirements: Regulatory bodies often require banks to hold certain types of assets, including high-quality bonds, as part of their regulatory capital requirements. Bonds are typically considered less risky assets compared to loans, so holding bonds can help banks meet regulatory standards for capital adequacy.

-

Asset-Liability Management: Banks use bonds as part of their asset-liability management strategy. Bonds with specific maturity dates can be matched with liabilities, such as customer deposits or long-term borrowings, to manage interest rate risk and ensure that the bank’s assets and liabilities are properly aligned.

-

Collateral: Bonds can also serve as collateral for various transactions, including borrowing from central banks or other financial institutions. Banks can pledge bonds as collateral to obtain funding or liquidity in times of need.

Overall, holding bonds in their assets allows banks to manage risk, generate income, meet regulatory requirements, and effectively manage their balance sheets. Bonds play a crucial role in the overall investment strategy and risk management practices of banks.

Reclassifying

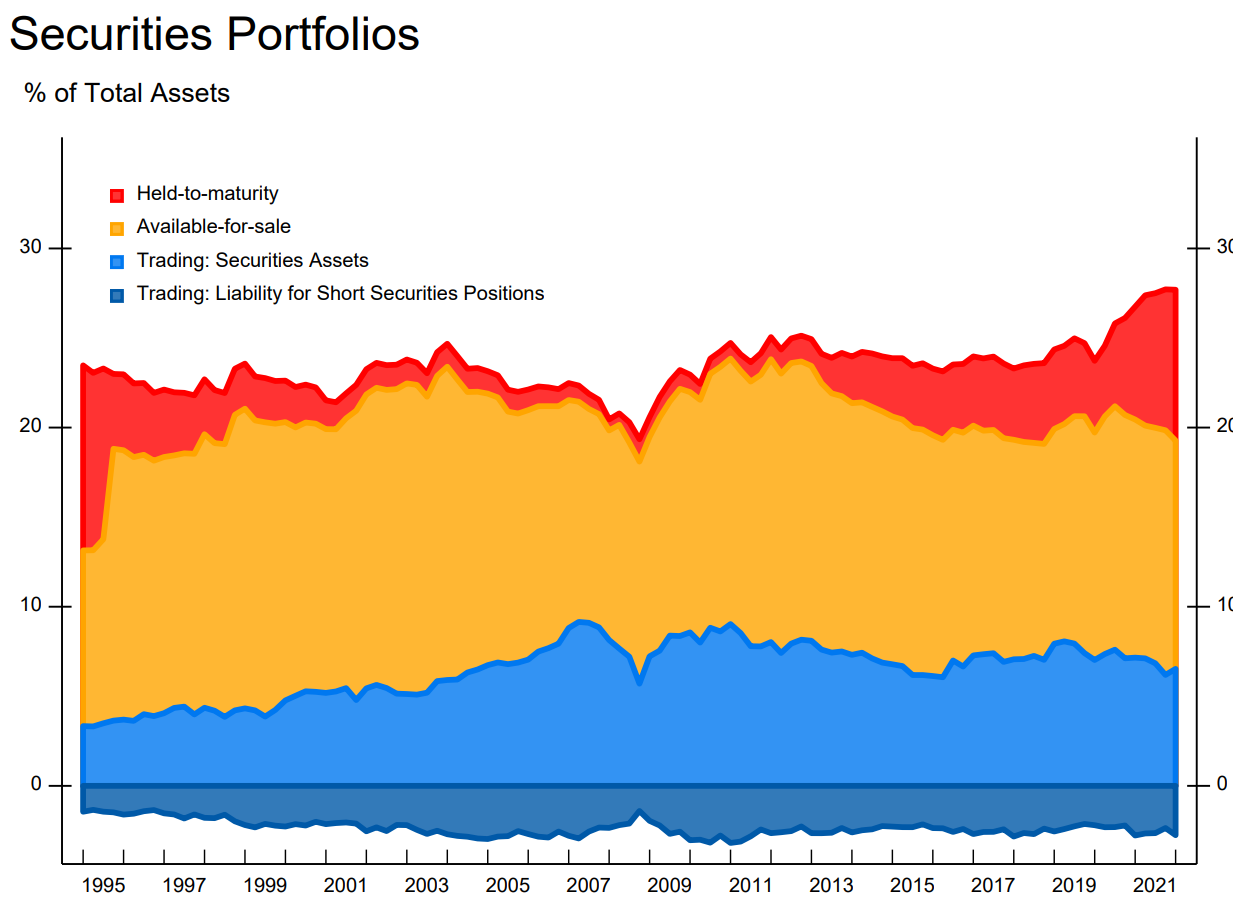

Since AFS is a catch-all category, that means that banks can move assets in or out of the AFS to the other ones when the intent has changed. For example, HTM to AFS and vice versa. Why? Mostly to stablize capital adequacy ratio and to stablize earnings.

Notice in the chart the HTM (red) has more than doubled in size as a percentage of all bank assets over the past several years.

Notice in the chart the HTM (red) has more than doubled in size as a percentage of all bank assets over the past several years.

A key difference between HTM and AFS is the accounting treatment of gains and losses as described at the begnning of the post. The gains and losses in the value of HTM that result from market movements (e.g., interest rates) aren’t recognized unless the asset is sold.

For AFS securities, however, such shifts in value, while not affecting accounting income, do affect the measurement of regulatory capital adequacy for large banks under the Basel III framework (for so-called “advanced approaches” firms).

On Oct 11, 2013, the Federal Register, published by the Department of Treasury and the OCC, wrote “[…] consistent with Basel III, the agencies and the FDIC proposed to require banks to include the majory of AOCI components in common equity tier 1 capital.”

Then it went on to say that they received a significant number of comments on the proposal to require banks to recognize AOCI in common equity tier 1 capital. Interestingly, the comments expressed concerns that became reality:

”[…] the change would introduce significant volatility in banks’ capital ratios due in large part to fluctuations in benchmark interest rates, and would result in many banks moving AFS securities into HTM or holding additional regulatory capital solely to mitigate the volatility resultingfrom temporary unrealized gains and losses in the AFS securities portfolio.”

The commenters also asserted that the change would likely impair lending and negatively affect banks’ ability to manage liquidity and interest rate risk and to maintain compliance with legal lending limits.”

In 2014, Bloomberg reported that JMPC and Wells Fargo are leading a shift in how banks account for their bond investments after a $44 billion plunge in value exposed a potential drain on capital under new rules. It also reported that The largest U.S. lenders are moving assets into HTM instead of designating them as AFS.

Unanswered questions

-

AFS as a whole decreased the most (slope the steepest) after 2003 until the GFC. Was it due to rising rates of that period? If it was due to rising rates, then we expect to see reduced AFS in 2022 as the Fed has been increasing rates. Indeed, even with 1 quarter of the data in 2022, we see that AFS has dropped. We will find out more when the new quarterly reports comes out.

-

Transfering assets from AFS to HTM can educe the volatility of regulatory capital ratios. However, the move will limit banks’ ability to sell those securities in the future. What does that mean for risk management and profitability of the banks? Would it affect negatively banks’ ability to manage liquidity and interest rate risk since banks won’t be able to sell from HTM?

-

I am curious as to if there are follow-up studies especially quantitatively on some of things raised in Federal Register / Vol. 78, No. 198 / Friday, October 11, 2013 / Rules and Regulations. Specifically, banks’s comments of concerns of aggregate impact of Basel III rule changes regarding the potential aggregate impact of the banks and the overall U.S. economy. Many commenters argued that the new rules would have significant negative consequences for the financial services industry. According to the commenters, by requiring banks to hold more capital and increase risk weighting on some of their assets, as well as to meet higher risk-based and leverage capital measures for certain PCA categories, the new rules would negatively affect the banking sector: restricted job growth; reduced lending or higher-cost lending, including to small businesses and low-income or minority communities; limited availability of certain types of financial products; reduced investor demand for banks’ equity; higher compliance costs; increased mergers and consolidation activity, specifically in rural markets, because banks would need to spread compliance costs among a larger customer base; and diminished access to the capital markets resulting from reduced profit and from dividend restrictions associated with the capital buffers. The commenters also asserted that the recovery of the U.S. economy would be impaired by the new rules as a result of reduced lending by banks that the commenters believed would be attributable to the higher costs of regulatory compliance. In particular, the commenters expressed concern that a contraction in small business lending would adversely affect job growth and employment.

-

From the same Federal Register, are the competitive concerns warranted? “[…] would create an unlevel playing field between banking organizations and other financial services providers.” Credit unions, foreign banks with significant U.S. operations, members of the Federal Farm Credit System, and entities in the shadow banking industry, and unregulated NBFIs, would have a competitive advantage over banking organizations as they are not subject to the new rules. The data seems to support these claims.

-

The new rules certainly increased complexity and implementation costs for large banks: software upgrades for new internal reporting systems, increased employee training, and the hiring of additional employees for compliance. Is it true that “a simple increase in the minimum regulatory capital requirements would have provided increased protection and increase safety and soundness without adding complexity to the regulatory capital framework”?

Reference

Federal Reserve Supervisory Policy and Guidance Topics on Accounting

Federal Register / Vol. 78, No. 198 / Friday, October 11, 2013 / Rules and Regulations

Available for Sale? Understanding Bank Securities Portfolios

Bloomberg: Banks Averting Bond Losses With Accounting Twist: Credit Markets